The Foundation for Peer to Peer Alternatives

P2P Social Currency (Money 2.0)

Hi there,

I would like to present the ideas in this article below for discussion with folks on this forum.

The article itself is something I put together over night but I have been sitting with the ideas for a couple years now.

I could be a lot more elaborate in my presentation of these ideas, but I thought I'd run it by other curiously minded folks, to have some critical feedback points, prior to putting significant energy into it...

With that said, please enjoy and comment as appropriate.

Original URL: http://evolvingtrends.wordpress.com/2008/10/21/p2p-social-currency-...

P2P Social Currency (Money 2.0)

October 21, 2008 at 7:18 pm

Premise:

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Dialog:

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of money that I give to my kids (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

In my opinion, the concept of “credit” and “credit rating” is good but the concept of interest is not. What I mean is that people and businesses should have a credit rating but it should be tied to something other than their ability to pay interest on money borrowed.

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated by how much you’ve lent others and how much time you’ve given people to pay you back, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

I would like to present the ideas in this article below for discussion with folks on this forum.

The article itself is something I put together over night but I have been sitting with the ideas for a couple years now.

I could be a lot more elaborate in my presentation of these ideas, but I thought I'd run it by other curiously minded folks, to have some critical feedback points, prior to putting significant energy into it...

With that said, please enjoy and comment as appropriate.

Original URL: http://evolvingtrends.wordpress.com/2008/10/21/p2p-social-currency-...

P2P Social Currency (Money 2.0)

October 21, 2008 at 7:18 pm

Premise:

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Dialog:

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of money that I give to my kids (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

In my opinion, the concept of “credit” and “credit rating” is good but the concept of interest is not. What I mean is that people and businesses should have a credit rating but it should be tied to something other than their ability to pay interest on money borrowed.

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated by how much you’ve lent others and how much time you’ve given people to pay you back, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

Views: 2104

Replies to This Discussion

-

Permalink Reply by Evolving Trends on

-

That's really good news, that others are thinking ambitiously, too :) It's definitely time for big thinking.

My idea with the draft proposal is to vet it here and then turn it into a simulation/game ... and see how it works.

So far, I made a lot of progress but it's complexity is subtle enough that it really needs deep critical thought at every turn...

Waiting on demurrage discussion to resolve ...

Thanks for the links!

-

-

My take on money definitions/models is that there will be MANY and there will be MANY communities each with a different money model.

The idea of Open Money (my take on it at least) is to provide a standard that enables porting of money from one model to another, so you won't get stuck in any model if you decide that it's not for you.

I doubt very much that there will be one model of money, but a common meta model will have to exist to enable trade between communities as well as porting of money (due to immigration of user) from one community to another.

-

Permalink Reply by Sepp Hasslberger on

-

you say "no harm done to the economy from individuals hoarding money (as people can create money by producing energy)..."

There is a hitch here somewhere.

You acknowledge elsewhere that money must circulate in the economy, like blood in the veins.

Hoarding will reduce the amount of money in circulation = it will hurt.

Making more money by making energy will heal the economy.

The trouble I see here is the following:

Too little money is bad for the economy and too much money is equally bad. Amount of money in circulation should be in a close relation to the quantity of goods/services to be exchanged. Hoarding unbalances in the direction of too little money. Creating more money may unbalance in the direction of too much money in circulation.

There should be a mechanism in any monetary system that adjusts - preferably automatically - the amount of money in circulation to the size of the economy.

You say hoarding is no problem because no one will wish to hoard their money when they could lend it out to gain points and make more. That is a view to be tested, and perhaps some thought should be given to having a regulating mechanism that prevents gross imbalance between the money supply and the size of the economy just in case that view turns out not to have been accurate.

The imbalance could also be too much money from too much energy production or it could simply be a question of not being able to adjust to a changing size of the economic base.

Demurrage allows you to contract the money supply, should such contraction be needed, by pulling money out of circulation.

You only have a provision for increasing the money supply (make more energy) but not for decreasing the supply once it is in circulation.

-

-

Awesome.

The imbalance could also be too much money from too much energy production or it could simply be a question of not being able to adjust to a changing size of the economic base.

Demurrage allows you to contract the money supply, should such contraction be needed, by pulling money out of circulation.

You only have a provision for increasing the money supply (make more energy) but not for decreasing the supply once it is in circulation.

>>

I want to clarify that the cap on hourly energy production per peer does limit money production by tying it to actual demand for energy ...

If energy production per peer had a dynamic cap on it (tied to demand for energy) then how will you get excess money created? If person A produces 10 megawatts of power and gets paid 10 Peer Dollars (I'm making the ratio up) and person B buys 10 megawatts of power (to supplement their energy production to meet unexpected or growing need or maybe they don't produce energy) then Peer Bank takes money from person B and hands it to person A and there is no new money created. If everyone becomes a producer of energy then you can have a situation where there is very little demand for energy from Peer Grid and so the cap per hour per peer for energy production is reduced to meet not exceed the reduced demand and so no new money will be created.

New money will only be created to fill Peer Grid with enough energy as a buffer for future demand but that buffer is limited in size. The process of filling Peer grid's energy buffer is the only process that can generate new money buy paying energy producers in expectation of future demand, but once the buffer new money creation stops and Peer Bank starts acting as a monetary transfer hub (not a physical energy hub) for p2p exchange of money for energy or energy for money.

The new money created, if it's hoarded will indeed be a problem, because it needs to be used (via lending, purchases of good and services and investment in appreciable assets) but if some people decide to save all their money then they either starve, have no clothes or have no life, and how many people do that given that money saved does not grow in value at all and does lose value relative to the growing economy.

The basis premise for having Peer Credits instead of demurrage and not in addition to is that people will lend, buy and sell to grow their wealth. Peer Credits exist as a carrot to encourage lending and selling/production of goods and services and do you really need a stick, too, e.g. demurrage?

People normally save their money until they have enough to buy a certain asset without borrowing, but when they can borrow with no interest from 1,000 peers at once then why should they save? The only reasons to save are: A) a reasonable security buffer (OK), or B) ignorance (Not OK) or C) disruptive intent (Not OK). So people who save too much money, i.e. savings beyond what is a reasonable security buffer (which is a psychological safety net not an actual needed one), those excessive savings can be subject to demurrage.

Does that sound like a good plan?

-

-

"New money will only be created to fill Peer Grid with enough energy as a buffer for future demand but that buffer is limited in size."

Hmmm - that's even worse than I thought. You have no real mechanism for injecting money into the system to take care of growing need for money, except a very approximate need to fill the energy buffer.

"...but if some people decide to save all their money then they either starve, have no clothes or have no life, and how many people do that given that money saved does not grow in value at all and does lose value relative to the growing economy."

Some people may save half their money and it will still be a problem. Money must stay in circulation and you have only a relatively tasteless carrot to make sure it does.

Let's clear up that question of money losing value relative to the growing economy. It's true that the economy can grow, but money value is a question of buying power. Are you suggesting that money generally will lose buying power as the economy grows?

"So people who save too much money, i.e. savings beyond what is a reasonable security buffer (which is a psychological safety net not an actual needed one), those excessive savings can be subject to demurrage."

I think that's a positively bad idea. First off - who decides what is a reasonable buffer. Secondly, why would you punish someone who decides to save up until they can make a large purchase - like buy a house or start a business - and who would likely exceed the limit considered reasonable amount of savings?

Clarification: Demurrage is not a punishment. It is a tool that allows to regulate total monetary mass and tends to prevent accumulation. Its general use is painless, especially if everyone benefits from the money collected by demurrage being re-distributed.

You still have no good mechanism that allows growth of monetary mass in response to growth of the size of the economy the system serves, and shrinking of the monetary mass in response to a shrinking economic base. There is a real need for both.

p.s. I'll be off for a few days - family affairs to take care of :)

-

-

You have no real mechanism for injecting money into the system to take care of growing need for money, except a very approximate need to fill the energy buffer.

>>

Why do you need to inject money in the system more than the need to drive productivity, which is done through the injection of energy...

?

Money must stay in circulation and you have only a relatively tasteless carrot to make sure it does.

>>

Taste is subjective. Credit points are very tasty to me. But if they're not tasty to you, they may not be tasty to others.

So then as I said before to discourage excessive saving (beyond some psychological safety buffer) you could use demurrage but that's a limp stick if you think credit points are a tasty carrot. In other words, two methods are better than one if each method's appeal is subjective, which is what our arguing here proves. I think demurrage is a limp stick, useless, and you think credit points is a tasteless carrot, useless. Together they may be more useful.

Let's clear up that question of money losing value relative to the growing economy. It's true that the economy can grow, but money value is a question of buying power. Are you suggesting that money generally will lose buying power as the economy grows?

>>

If wealth accumulation happens through accumulation of appreciable assets then yes, as assets appreciates money will lose buying power if it doesn't appreciate too, i.e. if it just sits there.

"So people who save too much money, i.e. savings beyond what is a reasonable security buffer (which is a psychological safety net not an actual needed one), those excessive savings can be subject to demurrage."

I think that's a positively bad idea. First off - who decides what is a reasonable buffer. Secondly, why would you punish someone who decides to save up until they can make a large purchase - like buy a house or start a business - and who would likely exceed the limit considered reasonable amount of savings?

>>

Regarding the first point, that's why it's better to let people save until they realize that saving money does not help them. But if we were to design a more proactive system, we'd have something to encourage people not to save too much money. Too much can be decided based on size of household. I mean who decided taxes? The government does. In this case, Peer Bank sets a limit on how much a given household/business can save, and that varries based on household/business size. It is bad because being proactive is bad. But that's the line of thought behind demurrage, i.e. to be proactive about making sure people don't save up too much money and slow down the flow of money. So you argue for demurrage but how do you apply demurrage? to all savings?

Why not let people save enough buffer to allow them to buy food etc while arranging for loan or getting their energy production capacity increased. And back to demurrage being bad, IMO, why not let people save, period. It only hurts them long term not to invest the money into assets or create more money thru credit points.

Secondly, why would you punish someone who decides to save up until they can make a large purchase - like buy a house or start a business - and who would likely exceed the limit considered reasonable amount of savings?

>>

They can borrow money from 1000s of peers at once. Why save up for something when you can get an interest free peer loan?

Its general use is painless, especially if everyone benefits from the money collected by demurrage being re-distributed.

>>

To take away something from one person and gives it to another is against one of those ideals. Those are the basic principles, and every model has to have some. I like demurrage without re-distribution (money goes back to Peer Bank and used as new money again) and that's in conjunction with credit points.

You still have no good mechanism that allows growth of monetary mass in response to growth of the size of the economy the system serves, and shrinking of the monetary mass in response to a shrinking economic base. There is a real need for both.

>>

The growth of monetary mass is tied to growth in productivity level which is tied to growth in energy supply. The abundance of energy increases productivity (as energy is converted into work) and monetary mass (as money is printed in return for peer energy production.)

If you have another need to grow monetary mass other than productivity then let me know what that is! As productivity increases the monetary mass is increased and assets appreciate as productivity grows. It's really a productivity based model.

-

-

P2P Social Currency (v0.09)

Changes from 0.08:

- Added section: Achieving Comparative Economic Advantage

- Clarified how Peer Credits help the seller make more money (last paragraph under Peer Loans)

- Added section: Why Money Hoarding is Useless

- Added section: Interoperability Model

- Updated section: Context

Notes:

This version still lacks a comprehensive narrative/story under Context. Also, need to articulate the design behind the design.

Draft of P2P Currency Proposal: v0.09

Premise

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Context

The “P2P Social Currency” as it’s defined here is an ambitious idea, or “thought model,” for what we may end up with in 20 years from now, not a plan for today. Its goal is to stimulate and challenge people to think different.

The idea is to get the assumptions of this model vetted by all willing brains out there and then

This is only a draft and a fuller article is on the way.

Objectives

At the core of this proposal are these critical objectives:

1. Enable a lending model that rewards the lender without punishing the borrower by rewarding lending with seller credit points that give the lender higher rating among sellers (of goods and services.)

2. Encourage P2P energy production and energy abundance by tying centralized money creation to P2P energy production, such that those who produce energy locally (from natural, abundant sources like solar and wind) get the then-equivalent in P2P currency (or Peer Dollars) from the P2P Central Bank (or Peer Bank, the distributed utility company) while those who consume energy get to benefit from low-priced, abundant energy.

3. Provide a multi-dimensional value system for the purchase of goods or services instead of the 1-dimensional value system we have today, which is the numerical cost of goods and services. So that consumers become not just price conscious but more conscious about the other values, e.g. seller’s support for environment, seller’s use of organic ingredients, seller’s credit points (or generosity in lending), etc.

Original Idea

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of a daily/weekly/monthly amount of my own money that I let my kids use (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, e.g. buying $1,000 for $1,110, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated on how much you’ve lent others and how much time you give people to pay you back before you report their defaulting, i.e. the grace period, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

Follow-up and Clarification

I should add a clarification here that the conditions/rules imposed on the exchange of this new money (as defined in this post) do not last beyond the singular transaction. In other words, if I restrict my money to spend itself on organic food only, the grocery store that sells me the organic food will no longer have those rules imposed on the money I paid to them. They can enforce their on rules on it, whatever they may be, and then use it to buy stuff with, and so on…

As to the 1-dimensional value system that is imposed by the current definition of money, i.e. the numerical (or “price”) value, I think it is only a matter of time before this value system goes from being 1-dimensional to N-dimensional. The reason the value system that is imposed by the current definition of money is limited to just the numerical dimension, i.e. price, is because it is assumed that people do their own research/homework when trading with others and make their decision to trade based on that. What I’m suggesting is for the new money to have more than just a numerical value for a value system, i.e. other values that are programmed/re-programmed into it by every user of that money, thereby allowing the automation and streamlining of trading decisions.

The key argument here, besides the point about the need to abandon “interest,” is that the value system that is ‘explicit’ in the definition of money is 1-dimensional, i.e. the “price,” or numerical value, and there is no excuse for having this 1-dimensional value system when we have computers, the Internet and the ability to implement an _explicitly_ multi-dimensional value system as the basis for a new, social, P2P currency.

The Origin of the Idea for Tying P2P Currency to P2P Energy

A very interesting idea suggested by Michel Bauwens of P2P Foundation is to derive the numerical value for this new money from the energy each person is able to produce (see: P2P energy.)

More on the Connection between P2P Currency and P2P Energy

There is a movement towards a Smart [Electric Distribution] Grid that allows individuals to produce electricity to power their homes and then send the extra capacity to the grid for others to use, and get paid for the energy they send into the grid.

The idea for Peer Energy Production will take some time to mature but there are already localized implementation of Smart Grid that allow businesses to play the role of a small electric utility.

So taking the Smart Grid further, we say that since solar energy is abundant then why not use this abundant resource that anyone can produce to be the basis for the new money. Meaning: if I can produce 100MegaWatts and push that into a ‘Peer Grid’ then the ‘Peer Bank’, which can print virtual Peer Dollars, would pay me 100 Peer Dollars or whatever amount, based on how much each Watt of energy goes for, which gets cheaper and cheaper the more energy is pushed into Peer Grid.

So the reason for tying money creation to energy creation is to encourage the generation of energy by people/businesses such that we end up with an abundance of energy as people exchange their excess locally generated energy for Peer Dollars, which, in the envisioned P2P Economy, they can use to buy anything with or lend to others.

There may need to be a cap put in place on how much energy a given party can produce so as not to allow one party or few parties to pump so much energy into Peer Grid as to bring energy price down for all other producers. Maybe a maximum on the amount of energy you can pump into the grid per hour has to be calculated based on demand. This is in addition to regulating the value of Peer Dollar relative to the energy, so that energy can become cheap as it becomes abundant, but not so cheap that it removes economic incentive for its production. Both have the effect of stabilizing the price of energy and the value of the currency.

There probably also needs to be an anti-aggregation provision (in the model) to disallow emergent master-slave behavior where one person or entity end up running a colony of P2P energy producing peers.

Achieving Comparative Economic Advantage

Since there is a cap on how much energy (per hour) a peer can pump into Peer Grid and since everyone who can produce energy is likely to maximize their contribution to Peer grid to make money, it is unlikely that significant comparative economic advantage can be achieved by one peer over others using energy product alone. The peer will have to compete for credit point (Peer Credits) by lending money to others and then use those Peer Credits to position themselves higher in the list of sellers for whatever good or service they produce (or resell). Another longer term way of achieving significant comparative economic advantage is to put money earned into assets that tend to appreciate as the economy grows, e.g. land or real estate.

Why Money Hoarding is Useless

Since interest does not exist in this model, money will not grow on its own as it does today, e.g. sitting in a bank. Given that, the only other reason to hoard money is security. But given that money loses its value if it’s not growing, and given that Peer Dollars are basically smart money that can actually alert its user (through email, messaging, etc) to the fact that it’s losing value by just sitting there :-) I doubt very much that participants in this model will have any desire to hoard money.

Given that only two ways exist for achieving significant comparative economic advantage:

1) accumulation of Peer Credits (through lending) combined with production of goods or services, and/or

2) investing in assets that appreciate, e.g. land or real estate

Participants in this mode are more likely to lend their money or invest it in appreciable assets, both of which are good for growing the economy.

Peer Loans

Why do we need to lend? Because we need money to flow in the system, like blood flowing in our veins. No blood/money flowing means death of the system. Lending is needed beyond the exchange of goods/services for money. That’s because in order to create or buy goods/services people need money and lending allows people to have more money than they can have from their labor. In other words, the increased flow of money through lending is important to the healthy functioning and growth of the system. The problem with “interest” being the incentive for lending today is that it’s used to derive more money for the lender, which has nothing wrong with it, at the expense of the borrower, which is wrong.

That is to say that “interest” rewards lenders and punishes borrowers. What we need is a replacement of interest as an incentive for lending. Something that would reward lender with punishing the borrower.

If someone lends money and instead of getting more money back they get good will points (Peer Credits) then more people will buy from that lender (the one with most Peer Credits), so the lender makes more money by selling *more* products and services, not by simply sitting back and collecting from borrowers.

The Peer Credit rating directly affects the position of the seller in the list of sellers for a given product or service. When buyers search for a given product or service, the seller with highest number of Peer Credits shows up on top.

Credit Points For Lenders

To encourage the flow of capital in the P2P economy, lenders need to have an incentive.

The incentive in this model is based on the assumption that in the P2P economy everyone is a buyer and a seller (of goods and/or services.)

The idea is to give lenders credit points (Peer Credits) that rank them higher as sellers when buyers search for goods or services that they happen to offer. The number of Peer Credits a lenders gets is based on how much they’ve loaned to others and their standard grace period (for loan repayment.)

Credit Points for Borrowers

When borrowers borrow money (Peer Dollars) under this model and repay it on time they do not gain credit points. The borrower’s benefit comes from having to pay no interest on money borrowed. If the borrower does not pay the borrowed amount after the grace period they get negative Peer Credits. However, the borrower can come out of a negative Peer Credit rating simply by lending lending money to someone else, after paying back the money they owe. While this may sound pessimistic for such borrowers, the ease with which people can accumulate money through the local production of energy (by pumping excess locally generated energy into Peer Grid and receiving the then-equivalent in Peer Dollars) should make it viable for borrowers to recover from negative Peer Credit rating.

The amount a borrower can borrow is directly tied to the number of Peer Credits they have, and since Peer Credits can only be obtained via the act of lending, this encourages people to keep lending and at the same time forgives people who fail to pay back borrowed money by giving them a chance to make money (by pumping excess locally produced energy back to Peer Grid) and then lend some of that money to someone else and keep doing that until they’ve established good Peer Credit rating.

The way the current system works is by penalizing borrowers who default without giving them an easy enough way to recover from their defaulting position. Furthermore, paying back the lender, after defaulting never helps the credit score, and borrowers are forced to borrow more rather than lend more because it’s assumed that money is scarce and cannot be peer produced, which is not the case in this proposed model) and borrowing more has the effect of concentrating money and power in the hands of the biggest lenders, instead of encouraging every borrower to become a lender, too, which is what this model aspires to do and which creates money for all puts power with the whole.

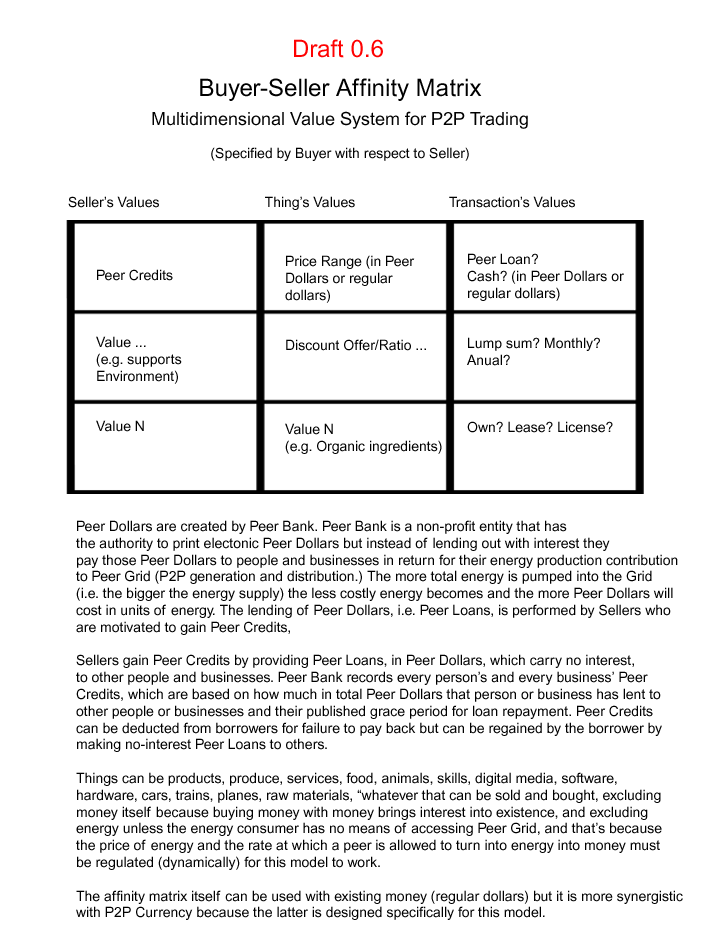

Affinity Matrix for P2P Trading

The Affinity Matrix allows the explicit definition of a multidimensional value system per each transaction involving Peer Dollars, but it should also be usable with conventional currency.

The affinity is asymmetric in nature, i.e. specified by buyer with respect to seller, and it applies only to goods and services, which do not include money because you shouldn’t be able to buy money with money as money as that would be equal to ‘interest,’ and which do not include or energy, except where the energy consumer cannot tap into Peer Grid, and that’s because the price of energy and the rate at which a peer is allowed to turn into energy into money must be regulated (dynamically) for this model to work.

The reason the affinity is unidirectional from buyer to seller is because the buyer holds money and the seller holds goods and/or services. The money has an objective value, i.e. the price, ($5 is $5 is $5) and the goods/service has a subjective value. The value of something, other than money, is ultimately subjective. In fact, that is why the Affinity Matrix is needed, i.e.: to add explicit subjective values to goods and services.

So given that goods and services have a subjective value (or values) and money has an objective value (price) the seller (or holder of goods and services) is not in position to dictate which buyer’s money they like to take. The reason being that you can’t have power in deciding a trade without having objective value in what you’re offering to trade. Your goods and services can have an extremely high subjective value but you can’t go to the bank and exchange them for money. If no one wants to buy your goods and services, no matter how good they are, you can’t make any money on them. Furthermore, if buyers decide to sit out the shopping season you can’t turn your goods and services into money. The buyer, on the other hand, is the holder of the money and given money has an objective value, which means that there is always someone willing to take it in return for goods or services. Therefore, the buyer has the power to dictate which seller’s goods and services they want to exchange their money for. The seller doesn’t except in cases where they have a monopoly on goods or services and those goods and services happen to be in demand. The seller is otherwise just happy to find a buyer to make a living off their trade. But if your goods and services are in high demand then you can decide which buyer’s money to take and the way to do that in a fair way is to offer it to the highest bidder. Otherwise, you risk starting a fight amongst the buyers and between buyers and yourself. Under the proposed model, sellers can price their items as high as they want and if that item is scarce or in very high demand then buyers will likely pay the price, assuming the seller and their goods and services have a high enough degree of affinity with the buyers’ values or the buyers, under conditions of scarcity, just don’t care about enforcing their values.

See: Buyer-Seller Affinity Matrix: Multidimensional Value System for P2P...

Interoperability Model

Given that there are many efforts now, mostly under the radar, to define various community currencies, it is obvious to me that we will have many “money models.” So the question becomes how to make all these models inter-operate, so that people can port their money out of one community into another, and so that inter-community trading becomes possible.

It is possible but it requires collaboration and, more importantly, orchestration.

I encourage those interested in defining community currency models to think differently and not follow ‘group think’ as that leads to reinforcing assumptions that maybe wrong. After all, even the geniuses who designed and evolved the current money system (sarcasm) were proven flawed in their assumptions.

Diversity of community currency models is not only essential it’s inevitable.

So there is definitely a need for an interoperability model that is thin and flexible enough to work with just about any model.

Open Feedback Request

I’m interested in counter-arguments, notes of caution and other critical feedback, pulled from failed historical attempts, present efforts or from thin air. This model still needs to be vetted rigorously before any effort is put into coding a simulation.

{kind=link}

-

-

"But given that money loses its value if it’s not growing, and given that Peer Dollars are basically smart money that can actually alert its user (through email, messaging, etc) to the fact that it’s losing value by just sitting there :-) I doubt very much that participants in this model will have any desire to hoard money."

I don't quite understand ... How does money lose value if it is just sitting there?

What would prevent me from accumulating money on my account as a savings for the future?

Is there any mechanism in the model by which the money gradually loses value?

(apart from not being used to gain points by lending)...

-

-

I meant lose its value as a measure of wealth relative to wealth accumulated by others in the form of appreciating assets ... the only way to grow wealth is to buy appreciable assets, e.g. land, buildings, etc This should be noted clearly in the draft under Accumulation of Wealth

I agree with the suggestion to have demurrage but only for savings that are bigger than some psychological security buffer

-

-

On money and energy

We have a provision that money is created by selling locally produced energy to the grid.

"The idea for Peer Energy Production will take some time to mature but there are already localized implementation of Smart Grid that allow businesses to play the role of a small electric utility."

It is true that there are schemes that allow the selling of locally produced solar energy for example to the utilities, but for now, those schemes only work because there are laws that impose a duty on the utilities to pay a higher (arbitrarily set) price for the energy from renewable sources. What if those laws weren't there, or were to change?

This brings to mind a danger point for the whole scheme of basing the value of the currency on energy production. You already propose

"... There may need to be a cap put in place on how much energy a given party can produce so as not to allow one party or few parties to pump so much energy into Peer Grid as to bring energy price down for all other producers. Maybe a maximum on the amount of energy you can pump into the grid per hour has to be calculated based on demand. This is in addition to regulating the value of Peer Dollar relative to the energy, so that energy can become cheap as it becomes abundant, but not so cheap that it removes economic incentive for its production. Both have the effect of stabilizing the price of energy and the value of the currency..."

A horrible thought comes to mind: The P2P economy and P2P money won't exist in a vacuum. At least for energy, we also have to think of those outside the p2p economy whose business is the production of electricity.

Let's assume that a way is found to produce energy more cheaply than is possible today, and let's assume that there aren't any laws that require utilities to purchase individually produced energy at an arbitrarily set higher price.

Considering economies of scale will eventually bring energy price down, perhaps below the cost of distributed production, and perhaps even below the cap on energy price envisioned by you, how is this going to affect the p2p monetary system?

-

-

Let's think about it...

Great point re: the proposed model won't exist in a vacuum. In a simulated reality it will, but in actual reality it will not..... wooops.

:)

-

-

This is what I meant by saying THIS MODEL NEEDS TO BE VETTED .....

This is a big issue of course, not for the simulation but for the actual implementation in 10-20 or 30 years.

There are things that will happen in those 30 years that can give us ideas that we simply cannot predict.

Should we be worried about it now or should we be content with running a simulation in a vacuum to prove the core ideas and inspire others?

© 2024 Created by Josef Davies-Coates.

Powered by

![]()