The Foundation for Peer to Peer Alternatives

P2P Social Currency (Money 2.0)

Hi there,

I would like to present the ideas in this article below for discussion with folks on this forum.

The article itself is something I put together over night but I have been sitting with the ideas for a couple years now.

I could be a lot more elaborate in my presentation of these ideas, but I thought I'd run it by other curiously minded folks, to have some critical feedback points, prior to putting significant energy into it...

With that said, please enjoy and comment as appropriate.

Original URL: http://evolvingtrends.wordpress.com/2008/10/21/p2p-social-currency-...

P2P Social Currency (Money 2.0)

October 21, 2008 at 7:18 pm

Premise:

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Dialog:

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of money that I give to my kids (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

In my opinion, the concept of “credit” and “credit rating” is good but the concept of interest is not. What I mean is that people and businesses should have a credit rating but it should be tied to something other than their ability to pay interest on money borrowed.

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated by how much you’ve lent others and how much time you’ve given people to pay you back, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

I would like to present the ideas in this article below for discussion with folks on this forum.

The article itself is something I put together over night but I have been sitting with the ideas for a couple years now.

I could be a lot more elaborate in my presentation of these ideas, but I thought I'd run it by other curiously minded folks, to have some critical feedback points, prior to putting significant energy into it...

With that said, please enjoy and comment as appropriate.

Original URL: http://evolvingtrends.wordpress.com/2008/10/21/p2p-social-currency-...

P2P Social Currency (Money 2.0)

October 21, 2008 at 7:18 pm

Premise:

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Dialog:

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of money that I give to my kids (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

In my opinion, the concept of “credit” and “credit rating” is good but the concept of interest is not. What I mean is that people and businesses should have a credit rating but it should be tied to something other than their ability to pay interest on money borrowed.

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated by how much you’ve lent others and how much time you’ve given people to pay you back, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

Views: 2104

Replies to This Discussion

-

Permalink Reply by Dante-Gabryell Monson on

-

note: i meant, when talking about learning to evolve towards rhizomatic relationships, that we learn to surrender even to the potential that the drama of the other person facilitated by deconstruction our own - increasingly detached - presence may bring , which in itself may lead to further detachment of the other and of ourselves , can lead to an absence of shared presence, and leave us in nothingness / no shared space. - Hence a further adaptation leading to opening up more connections, and not being ( specifically ) dependent on any one person we have a relation with, while being dependent on all, and sharing with each other not based on a mutual conditional contract, but on increasing non-exclusive shared co-creative intention, with an opening to similar relations with others and in multiple realities, which very much requestions many of the socio-culture related to close relations, and can only build itself on unconditional love, opening to unlimited understanding, and further building presence and overcoming fear of falling back into contemplation into nothingness. - opening up to a variety of close relations to which we do not create a specific addiction to also further increases the speed of the mutual learning process, and the access to a number of "objects" related to the experiences of the other, including through energetical channels we open for each other.

-

Permalink Reply by Evolving Trends on

-

Dante,

You have a torrent of thought, not a stream, and I'm used to taking in a trickle from people.

So please don't mind if my responses are delayed :)

I do believe in what you're working for and I understand as well as value the position you're in at this time and I believe that the exchange is definitely beneficial to the dream we share with so many

I am just slow sometimes on responding because I am processing a great many ideas and problems at once.... Maybe I need to think of a way to take the "I" out of the picture or make it just one voice in the me, and be a good parent to all the sub-me's in me, including the "I" instead of continuing to fight for the "I" to have its say above all.

But while the "parent me" is working towards that sort of inner and outer governance of my 'child me's, including the "I", "I" want to clarify something about "trust", "morals", "ethics", "beauty", "friendship", "beauty", "love", "laws" ... The choices we make in these "non-computable value dimensions" cannot be or should not be computed by an algorithm or by any type of definable process. They require non-computable judgment or the "knowing" that we have as human beings. Maybe that "knowing" can be channeled into machines at some point in the future but we are not even sure about its source, and I'm definitely not conveying religious thought here, but in terms of plausible scientific theory of consciousness on the level of Penrose' OR (which I picked up from Pesinger's writings that Michel pointed me to)

The ideas of non-computable judgment or objective reduction had been with my "me" for a while now, when it comes to trust, beauty, choice etc

So the "trust matrix" becomes an "affinity matrix" since affinity (as defined in chemistry) can be computed.

Maybe the "I" in me is having it's last stand here ...

This discussion is definitely helping my "me" grow

But like I said, you have a torrent of thought and the "I" in me used to taking in a trickle at any given time

The "I" in me still wants to summarize to feel in control, so let it...

-

-

Please note the Images Only thread of the same name.

I've just posted an image that represents my comprehension/understanding so far of the concept of Multidimensional Value System for P2P trading, including P2P Currency, and how it's created and used within an ethically/morally positive economic system.

The image is the output of this 50+ reply creative-philosophical symbiosis (or brainstorming session)

I look forward to critical feedback and will be happy to answer any question about it

I hope to have an updated post soon with more diagrams

Thanks

-

-

Dante,

I would like to delete this current P2P Currency discussion (I saved all your responses on my laptop) and restart the discussion to focus on key issues with -and aspects of- the model itself.

Is that OK with you?

-

Permalink Reply by Josef Davies-Coates on

-

Please do not delete this discussion!

Lots of useful stuff said (and not even read yet) and I'm certain most people haven't saved local version on their own laptops.

Please do start new focussed discussions though!

Thanks,

Josef.

-

-

Thanks for noting that Joseph.

I've just updated the model under the Images Only thread.

Changes:

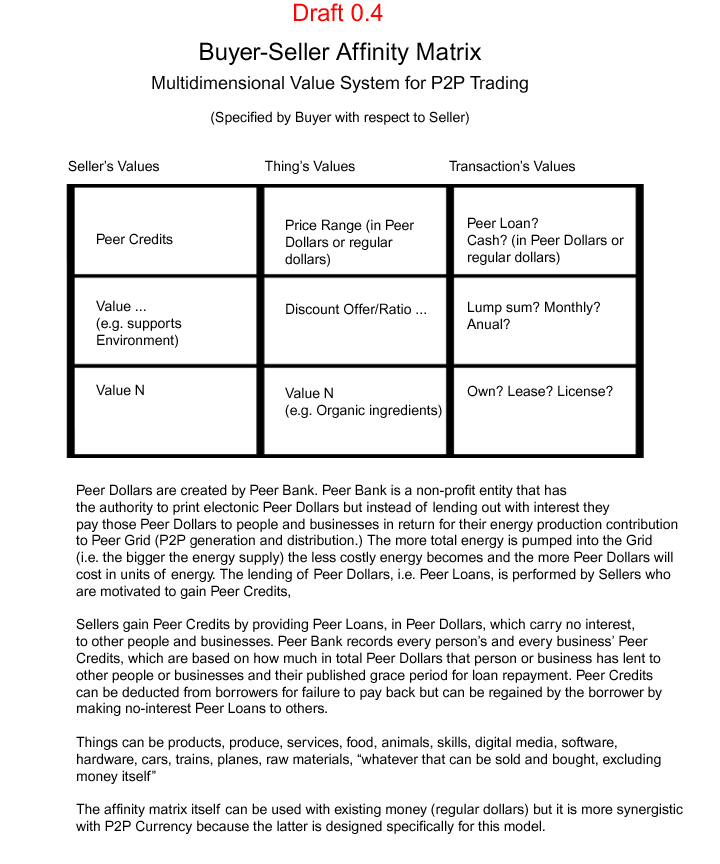

- Clarified "Cash" under Transaction's Values as Peer Dollars or regular dollars

- Clarified "Thing" definition to exclude money itself

- Clarified how to handle increasing abundance of energy supply (to avoid deflating value of money)

- Took away ability to provide Peer Loans by Bank and moved it exclusively to peers to let money supply be tied to peers' energy production exclusively. This is to prevent erosion of incentive for energy production by peers.

-

-

Abundance of energy supply (which is what future solar generation and smart peer grid technologies promise) is handled in the current draft of P2P Currency model by lowering the Peer Dollar equivalent per unit of energy, i.e. energy becomes cheap and abundant but buying power per Peer Dollar is not diluted

Also, just noticed Michel's post on Policy of Abundance etc which I'm sure connects to this discussion ...

-

-

Hi Marc,

I do not mind leaving all posts as an searchable archive ( non-linear entry points through search engines + place to refer back to some points we may have expressed )

But if you have specific reasons for deleting it, feel free to let me know the reasons, as I am not against deleting if it has a purpose that outweighs the benefits of leaving it available.

-

-

I was thinking that folks here may find the length and expansiveness of our discussion to be too distracting (away from the subject), as brainstorming usually is.

However, Joseph noted that he's interested in keeping these brainstorming notes, so that invalidated my original concern

I wish we had forum software that allowed us to architect the flow of conversation, so that we can have a more structured way of conversing and easier time extracting value from such expansive free-style discussions (see the post on Traffic Signs for Conversation Flow Management.. which could be a starting point for building such forum software)

But we could always summarize the ideas, thoughts and open questions as a mind maps and post them on the Images Only thread ... if it's needed

-

Permalink Reply by Michel Bauwens on

-

You should have a look at the structured discussions at Solutions Exchange in India, but it requires manpower.

They ask a question to the community, under the guidance of a facilitator, then at some point, the faciliator makes an executive summary for later user.

Michel

-

-

Draft of P2P Currency Proposal: v0.4

Premise

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Context

The “P2P Social Currency” as it’s defined here is “thought model” for what we might want to have in 20 years from now, not a blueprint for now. Its goal is to stimulate and challenge people to think different.

Having said that, the model described here can be combined with today’s money to move us towards a more conscious society.

Objectives

At the core of this proposal are these critical objectives:

1. Enable a lending model that rewards the lender without punishing the borrower.

2. Encourage P2P energy production (from home based solar/wind generators) by tying money creation to energy production.

3. Provide a more conscious, multi-dimensional value system for the purchase of goods or services instead of the 1-dimensional value system we have today, which is the numerical cost of goods and services.

Dialog

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of a daily/weekly/monthly amount of my own money that I let my kids use (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

In my opinion, the concept of “credit” and “credit rating” is good but the concept of “interest” is not. What I mean is that people and businesses should have a credit rating but it should be tied to something other than their ability to pay interest on money borrowed.

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, e.g. buying $1,000 for $1,110, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated on how much you’ve lent others and how much time you give people to pay you back before you report their defaulting, i.e. the grace period, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

Additional Clarification

I should add a clarification here that the conditions/rules imposed on the exchange of this new money (as defined in this post) do not last beyond the singular transaction. In other words, if I restrict my money to spend itself on organic food only, the grocery store that sells me the organic food will no longer have those rules imposed on the money I paid to them. They can enforce their on rules on it, whatever they may be, and then use it to buy stuff with, and so on…

As to the 1-dimensional value system that is imposed by the current definition of money, i.e. the numerical (or “price”) value, I think it is only a matter of time before this value system goes from being 1-dimensional to N-dimensional. The reason the value system that is imposed by the current definition of money is limited to just the numerical dimension, i.e. price, is because it is assumed that people do their own research/homework when trading with others and make their decision to trade based on that. What I’m suggesting is for the new money to have more than just a numerical value for a value system, i.e. other values that are programmed/re-programmed into it by every user of that money, thereby allowing the automation and streamlining of trading decisions.

The key argument here, besides the point about the need to abandon “interest,” is that the value system that is ‘explicit’ in the definition of money is 1-dimensional, i.e. the “price,” or numerical value, and there is no excuse for having this 1-dimensional value system when we have computers, the Internet and the ability to implement an _explicitly_ multi-dimensional value system as the basis for a new, social, P2P currency.

Another clarification is that if someone who has borrowed money does not pay back the money they get good will points taken out, much like the current credit rating system with the important exception that they can regain good will points (i.e. gain in their credit rating) by lending money to others rather than borrowing more money and paying interest on it.

A very interesting idea suggested by Michel Bauwens of P2P Foundation is to derive the numerical value for this new money from the energy each person is able to produce (see: P2P energy.)

Connection Between P2P Energy Production and Money Creation

There is a movement towards a Smart [Electric Distribution] Grid that allows individuals to produce electricity to power their homes and then send the extra capacity to the grid for others to use, and get paid for the energy they send into the grid.

The idea for Peer Energy Production will take some time to mature but there are already localized implementation of Smart Grid that allow businesses to play the role of a small electric utility.

So taking the Smart Grid further, we say that since solar energy is abundant then why not use this abundant resource that anyone can produce to be the basis for the new money. Meaning: if I can produce 100MegaWatts and push that into a ‘Peer Grid’ then the ‘Peer Bank’, which can print virtual Peer Dollars, would pay me 100 Peer Dollars or whatever amount, based on how much each Watt of energy goes for, which gets cheaper and cheaper the more energy is pushed into Peer Grid.

So the reason for tying money creation to energy creation is to encourage the generation of energy by people/businesses such that we end up with an abundance of energy as people exchange their excess locally generated energy for Peer Dollars, which, in the envisioned P2P Economy, they can use to buy anything with or lend to others.

Peer Loans

Why do we need to lend? Because we need money to flow in the system, like blood flowing in our veins. No blood/money flowing means death of the system. Lending is needed beyond the exchange of goods/services for money. That’s because in order to create or buy goods/services people need money and lending allows people to have more money than they can have from their labor. In other words, the increased flow of money through lending is important to the healthy functioning and growth of the system. The problem with “interest” being the incentive for lending today is that it’s used to derive more money for the lender, which has nothing wrong with it, at the expense of the borrower, which is wrong.

That is to say that “interest” rewards lenders and punishes borrowers. What we need is a replacement of interest as an incentive for lending. Something that would reward lender with punishing the borrower.

If someone lends money and instead of getting more money back they get good will points (Peer Credits) then more people will buy from that lender (the one with most Peer Credits), so the lender makes more money by selling *more* products and services, not by simply sitting back and collecting from borrowers.

Applicable Today

All concepts here can be implemented today using today’s money. There is no need to wait for P2P Energy/Peer Dollars. The only benefit (big benefit) of Peer Dollars is that they encourage P2P energy production. The model itself as described here is beneficial with or without P2P Energy/Peer Dollars, and can be applied today.

Images

1. Buyer-Seller Affinity Matrix: Multidimensional Value System for P2P Trading

-

-

Most of the changes in this v.05 are to the Objectives section.

This version still lacks a comprehensive narrative/story under Context

Draft of P2P Currency Proposal: v0.5

Premise

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Context

The “P2P Social Currency” as it’s defined here is an ambitious idea, or “thought model,” for what we may end up with in 20 years from now, not a plan for today. Its goal is to stimulate and challenge people to think different.

Having said that, the concept of multidimensional currency, as described here, can be used with today’s money to move us closer towards a conscious economy.

This is only a draft and a fuller article is on the way.

Objectives

At the core of this proposal are these critical objectives:

1. Enable a lending model that rewards the lender without punishing the borrower by rewarding lending with seller credit points that give the lender higher rating among sellers (of goods and services.)

2. Encourage P2P energy production and energy abundance by tying money creation to energy production, such that those who produce energy (from natural, abundant sources like solar and wind) get paid for it while those who consume energy get to benefit from cheap, abundant energy. This way the Central Bank (e.g. Federal Reserve) is replaced by a new kind of utility company (referred to here as Peer Bank.)

3. Provide a multi-dimensional value system for the purchase of goods or services instead of the 1-dimensional value system we have today, which is the numerical cost of goods and services. So that consumers become not just price conscious but more conscious about the other values, e.g. seller’s support for environment, seller’s use of organic ingredients, seller’s credit points (or generosity in lending), etc.

Original Idea

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of a daily/weekly/monthly amount of my own money that I let my kids use (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, e.g. buying $1,000 for $1,110, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated on how much you’ve lent others and how much time you give people to pay you back before you report their defaulting, i.e. the grace period, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

Follow-up and Clarification

I should add a clarification here that the conditions/rules imposed on the exchange of this new money (as defined in this post) do not last beyond the singular transaction. In other words, if I restrict my money to spend itself on organic food only, the grocery store that sells me the organic food will no longer have those rules imposed on the money I paid to them. They can enforce their on rules on it, whatever they may be, and then use it to buy stuff with, and so on…

As to the 1-dimensional value system that is imposed by the current definition of money, i.e. the numerical (or “price”) value, I think it is only a matter of time before this value system goes from being 1-dimensional to N-dimensional. The reason the value system that is imposed by the current definition of money is limited to just the numerical dimension, i.e. price, is because it is assumed that people do their own research/homework when trading with others and make their decision to trade based on that. What I’m suggesting is for the new money to have more than just a numerical value for a value system, i.e. other values that are programmed/re-programmed into it by every user of that money, thereby allowing the automation and streamlining of trading decisions.

The key argument here, besides the point about the need to abandon “interest,” is that the value system that is ‘explicit’ in the definition of money is 1-dimensional, i.e. the “price,” or numerical value, and there is no excuse for having this 1-dimensional value system when we have computers, the Internet and the ability to implement an _explicitly_ multi-dimensional value system as the basis for a new, social, P2P currency.

Another clarification is that if someone who has borrowed money does not pay back the money they get good will points taken out, much like the current credit rating system with the important exception that they can regain good will points (i.e. gain in their credit rating) by lending money to others rather than borrowing more money and paying interest on it.

The Origin of the Idea for Tying P2P Currency to P2P Energy

A very interesting idea suggested by Michel Bauwens of P2P Foundation is to derive the numerical value for this new money from the energy each person is able to produce (see: P2P energy.)

More on the Connection between P2P Currency and P2P Energy

There is a movement towards a Smart [Electric Distribution] Grid that allows individuals to produce electricity to power their homes and then send the extra capacity to the grid for others to use, and get paid for the energy they send into the grid.

The idea for Peer Energy Production will take some time to mature but there are already localized implementation of Smart Grid that allow businesses to play the role of a small electric utility.

So taking the Smart Grid further, we say that since solar energy is abundant then why not use this abundant resource that anyone can produce to be the basis for the new money. Meaning: if I can produce 100MegaWatts and push that into a ‘Peer Grid’ then the ‘Peer Bank’, which can print virtual Peer Dollars, would pay me 100 Peer Dollars or whatever amount, based on how much each Watt of energy goes for, which gets cheaper and cheaper the more energy is pushed into Peer Grid.

So the reason for tying money creation to energy creation is to encourage the generation of energy by people/businesses such that we end up with an abundance of energy as people exchange their excess locally generated energy for Peer Dollars, which, in the envisioned P2P Economy, they can use to buy anything with or lend to others.

Peer Loans

Why do we need to lend? Because we need money to flow in the system, like blood flowing in our veins. No blood/money flowing means death of the system. Lending is needed beyond the exchange of goods/services for money. That’s because in order to create or buy goods/services people need money and lending allows people to have more money than they can have from their labor. In other words, the increased flow of money through lending is important to the healthy functioning and growth of the system. The problem with “interest” being the incentive for lending today is that it’s used to derive more money for the lender, which has nothing wrong with it, at the expense of the borrower, which is wrong.

That is to say that “interest” rewards lenders and punishes borrowers. What we need is a replacement of interest as an incentive for lending. Something that would reward lender with punishing the borrower.

If someone lends money and instead of getting more money back they get good will points (Peer Credits) then more people will buy from that lender (the one with most Peer Credits), so the lender makes more money by selling *more* products and services, not by simply sitting back and collecting from borrowers.

Applicable Today

All concepts here can be implemented today using today’s money. There is no need to wait for P2P Energy/Peer Dollars. The only benefit (big benefit) of Peer Dollars is that they encourage P2P energy production. The model itself as described here is beneficial with or without P2P Energy/Peer Dollars, and can be applied today.

See: Buyer-Seller Affinity Matrix: Multidimensional Value System for P2P...

{kind=link}

© 2024 Created by Josef Davies-Coates.

Powered by

![]()