The Foundation for Peer to Peer Alternatives

P2P Social Currency (Money 2.0)

Hi there,

I would like to present the ideas in this article below for discussion with folks on this forum.

The article itself is something I put together over night but I have been sitting with the ideas for a couple years now.

I could be a lot more elaborate in my presentation of these ideas, but I thought I'd run it by other curiously minded folks, to have some critical feedback points, prior to putting significant energy into it...

With that said, please enjoy and comment as appropriate.

Original URL: http://evolvingtrends.wordpress.com/2008/10/21/p2p-social-currency-...

P2P Social Currency (Money 2.0)

October 21, 2008 at 7:18 pm

Premise:

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Dialog:

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of money that I give to my kids (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

In my opinion, the concept of “credit” and “credit rating” is good but the concept of interest is not. What I mean is that people and businesses should have a credit rating but it should be tied to something other than their ability to pay interest on money borrowed.

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated by how much you’ve lent others and how much time you’ve given people to pay you back, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

I would like to present the ideas in this article below for discussion with folks on this forum.

The article itself is something I put together over night but I have been sitting with the ideas for a couple years now.

I could be a lot more elaborate in my presentation of these ideas, but I thought I'd run it by other curiously minded folks, to have some critical feedback points, prior to putting significant energy into it...

With that said, please enjoy and comment as appropriate.

Original URL: http://evolvingtrends.wordpress.com/2008/10/21/p2p-social-currency-...

P2P Social Currency (Money 2.0)

October 21, 2008 at 7:18 pm

Premise:

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Dialog:

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of money that I give to my kids (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

In my opinion, the concept of “credit” and “credit rating” is good but the concept of interest is not. What I mean is that people and businesses should have a credit rating but it should be tied to something other than their ability to pay interest on money borrowed.

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated by how much you’ve lent others and how much time you’ve given people to pay you back, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

Views: 2104

Replies to This Discussion

-

Permalink Reply by Sepp Hasslberger on

-

"The new networked, programmable money should abandon the idea of paying interest on borrowed money."

Historically, it was well recognized that interest is pernicious. There have been several attempts to ban the taking of interest, even involving heavy penalties (examples are the Roman Catholic church and Islam) but they had little success.

Since interest is a reward for putting money back into circulation instead of simply holding on to it, and since the decision to loan out money putting it into circulation is a personal one, in order to abandon the idea of interest, the new system would have to supply a comparable advantage (or the avoidance of a comparable disadvantage) to stimulate the lending out of money into circulation rather than the holding of it in your possession.

A historic example of discussion of this dilemma is the work of Silvio Gesell, who chose avoidance of a comparable disadvantage as the tool to stimulate money circulation (loaning of money into circulation) without the 'carrot' of interest.

Gesell proposed a continuous but slight devaluation of circulating money by means of a fee ("demurrage") which is charged on the money and which supplies the stimulus to lend money and let others pay the fee, rather than hold on to it and pay it yourself. In a programmable money such as you propose, such a continuous periodic fee would be easy to implement.

The proceeds from demurrage would also be an easy source of money to do socially relevant things with. One thing would be to support families by distributing a share of this money to mothers with children (Gesell proposed that one).

Another would be to simply return the money to all participants in the system. This would have the effect of strongly countering the tendency of money to accumulate with those who already have a lot of it, since the charge depends on how much money you are hoarding (or using) and the distribution presumably would be one-for-one, i.e. regardless of how much money they have, each participant in the economic game would receive an equal share.

The percentage of demurrage would be low enough where it would not be a heavy burden (something like 1/2 of one per cent per month, or 6 per cent per year), but enough to counter-act the incentive of charging interest. The big difference would be that proceeds from demurrage, in contrast with proceeds from interest, would accrue to everyone rather than those who possess the most money.

Some links to articles discussing Gesell's proposal of demurrage or negative interest:

http://www.hasslberger.com/economy/eco_1.htm

http://www.hasslberger.com/economy/eco_2.htm

Book by Gesell: "The Natural Economic Order"

A discussion of the "Woergl experiment" by Silvano Borruso

-

Permalink Reply by Evolving Trends on

-

Hi Sepp,

The need to keep money circulating through lending (not only exchange of goods/services for money) is important (thanks for putting emphasis on it) and as such I added an explanation in the last couple versions of this draft (e.g. v0.5 under Peer Loans,) prior to your comment here, so your comment is totally in sync with where I was going in the last two drafts.

The idea I've tried to convey as a solution for giving comparable advantage to those who lend is to given them higher "credit points" which translate to higher ranking when they sell goods or services (excluded from goods and services is the generation of energy, which is exchangeable for Peer Dollars by Peer bank only, without regards to seller's credit points, and that's meant to encourage the production of energy by all and allow new participants the same opportunity as existing ones.) The idea of giving credit points to those who lend (based on amount of loan and grace period) is to reward generosity with the ability to make more money as a producer of goods and services. What is ASSUMED here is that in the future P2P Economy everyone will be a producer and a consumer, or Prosumer. So everyone stands to benefit from this new kind of credit system, where the incentive to lend will be having higher credit points to stand out among sellers, or High Seller Rank (just like Google's PageRank but based on how much you've loaned to others, your default grace period, etc)

What holes if any do you see in this logic?

(p.s. thanks for the references)

-

-

My thought in bringing in the possibility of demurrage was that perhaps the credit rating points would be too weak of an incentive for lending, but I may be stuck in the views of today's money with that observation.

Perhaps the multidimensionality of the money with its programmable spending preference will make the credit rating points a very alluring incentive to lend money.

I would be content to leave the determination of this to experimental verification.

-

-

Thank you for bringing up Demurrage.

Demurrage sounds like a punishing concept. It is OK to hoard money, IMO, because ultimately you can't constrain human nature and greed is a deeply programmed instinct.

If you don't lend money to others, in the proposed model of P2P _social_ currency, you just won't be able to grow your money as much if you were to lend to others because no one or very few will buy goods and services from you.

It's possible that you accumulate enough money from energy production and reuse the money you make from energy production to grow your energy production capacity and so on, until you become the biggest energy producer, but the safeguard for this in the proposed model is that the price of energy drops the more energy is pumped into the Peer Grid, so you'll hit a point at which energy you produce is not enough to sustain growth of your energy production capacity.

There may also needs to be a cap put in place on how much energy a given party can produce so as not to allow one party or few parties to pump so much energy into Peer Grid as to bring energy price down for all other producers. Maybe a maximum on the amount of energy you can pump into the grid per hour has to be calculated based on demand, to stabilize the price of energy, and the currency which is based on it.

As to the "mutual credit" idea mentioned in email chatter I received today, I tend to think that it is unfair for the seller to choose buyers based on their credit rating or any other value. That would be akin to discrimination. Buyers can discriminate based on seller's credit because buyers should be able to decide who gets their money. But sellers should not be able to decide who gets their product. It sounds asymmetric and unfair but listen to this example:

If I want to buy a mobile phone from a manufacturer that disposes of their toxic waste safely then I should be able to specify that in my money allocated to the purchase and let my money find such vendor and spend itself ... (note: in reality this involves programming the transaction not the money, so the money can be re-used with new criteria by the seller to buy other things, e.g. supplies)

But a mobile phone manufacturer should not be able to dictate that only White Republican Male should be able to buy their phones.

In our society today, a buyer choosing a seller based on criteria is OK, but not OK for seller to choose a buyer because that's taken as discrimination. The reason for this is due to the fact that that money is defined by law as universally exchangeable for any goods or service so if you have money, as a buyer, the seller should not restrict what you can buy except based on the actual price of goods/services they're offering.

If you are a buyer and you hold the money and you should be able to decide which goods/services to exchange it for because money is guaranteed by law to be exchangeable for any goods/services. However, if you're the seller, you hold the goods/services, and you cannot decide which money (or whose money) to exchange for them because goods/services are not guaranteed by law to be exchangeable for any money, i.e. as a seller the law does not give you the right to decide whose money to accept/refuse. As a buyer, using official or accepted currency, the law (or the model in this case) gives you the right to decide whose goods/service to exchange your money for.

It's an asymmetry that makes sense to me and as such I have healthy doubts about the mutual credit idea (or mutual affinity matrix, i.e. to go to a P2P Affinity Matrix instead of the asymmetric Buyer-Seller Affinity Matrix in the proposed model)

What do you (or what does anyone here) think about this argument for asymmetric multidimensional exchange?

-

-

"Demurrage sounds like a punishing concept. It is OK to hoard money, IMO, because ultimately you can't constrain human nature and greed is a deeply programmed instinct."

Yes, demurrage is a punishing concept, to limit undesirable behavior. I believe that it isn't really ok to hoard money as that tends to make the system unstable. Widespread hoarding would tend to make money scarce. Widespread spending of hoarded money would make money abundant. Cycles of relative scarcity and abundance are what has plagued the economy (and baffled economists) for quite some time.

So from a systems point of view, it would be preferable if money did not have a built-in capacity to allow widespread hoarding and sudden spending.

Human nature and greed, I believe, is an instinct that is honed by cyclic scarcity and abundance. In order to compensate for the effects of these swings on individual/family survival, you would tend to amass your own monetary cushion and greed would be the external manifestation of that desire. ("Saving for a rainy day" is the popular term, but greed is an extreme manifestation of that same desire.)

In a stable money system there would be no place and really no need for greed.

Asymmetric multidimensional exchange, i.e. buyer is perfectly free to choose what to spend his/her money on, and seller being prevented from discriminating who to sell his/her goods to is perfectly compatible with the current situation, which does not seem at all problematic.

-

-

Well, it's good that we're discussing the nature of greed.

I need to rephrase the part of my text that you've quoted because it should have context built into it. The context for that statement is the new model not the current model. It is OK to hoard money in the new model because everyone can make money buy simply pumping excess locally generated energy into the grid, while having a dynamic cap on how much energy you can convert to money per hour and having energy price be dynamically regulated, too, to achieve stability. And the name of the game is not how much money you have but how many Peer Credits you have, because Peer Credits, which encourage production and reselling/distribution of goods and services by peers, and which have no cap, are the only way to achieve comparative advantage, and by definition Peer Credits enable the flow of money in the economy. So if you want to hoard money you don't stall the whole system, you only stall yourself.

Does that make sense to you?

-

Permalink Reply by Dante-Gabryell Monson on

-

small detail - there is also a wiki version of the book by Silvio Gesell:

"The Natural Economic Order"

http://wikilivres.info/wiki/The_Natural_Economic_Order

:-)

-

-

Unless you apply a specific argument/feature from Gesell's model to this debate, e.g. demurrage, I cannot debate it.

The reason is I want to remain detached from historical and existing definitions to retain my "zero gravity thinker" status, to help break out of 'group think' and to encourage diversity in models, which is inevitable.

The meta model (the model to bring all models together) would be of significant interest to me, and my remaining detached from existing and historical models will allow me to test the limits of any such meta model.

My observation so far is that being a zero-gravity thinker is not an easy job (except on this forum, which is great because people are so open minded here) and the reason it's not an easy job is because people in general will ultimately want you think in common, which is the cause of the cascade effect (search for Pesinger in this thread and follow Michel's link)

However, as I stated above, if you take an argument/feature from an existing/historical model and apply it to this discussion then I will definitely debate it and if it makes sense I would use it, but it has to make clear sense.

-

Permalink Reply by Chris Cook on

-

We are used to thinking that Money must necessarily be credit, as is our conventional money, which is created by credit institutions as interest-bearing loans.

In fact, while credit (aka time to pay) is a necessary part of a monetary system, credit need not -indeed, should not, IMHO, be "monetised".

By way of example, the WIR is a B2B barter exchange in Switzerland where billions of Swiss Francs' worth of goods and services change hands on credit terms. Defaults on debit balances are rare, because participants must give a mortgage over their property by way of security. ie the WIR is "property-backed"

The point is that no actual "fiat" Swiss Francs change hands in settlement of WIR credit. Instead, "money's worth" is exchanged by reference to Swiss Francs as a "Value Unit".

The actual economic value provided by banks is that of an implicit guarantee of the borrower's (or buyer's) credit, and any "interest" charged covers not only a payment to depositors, but also defaults and operating costs.

The approach I advocate is of mutually guaranteed "Peer to Peer" credit within the framework of a "Guarantee Society" consensual agreement. No interest is charged, but both sellers and buyers pay a service charge and a provision into a default pool operated (by a Service-provider-formerly-known-as-a-Bank) to support the use of the mutual guarantee. Users have guarantee limits, rather than credit limits, and may settle credit not just in conventional "fiat" money but in money's worth of goods, services, or other obligations (cf RipplePay).

The "Pool" is owned mutually, not by the Bank, as now.

In relation to "Money's Worth" I advocate the "Unitisation" of land rental values and of energy (in particular) within a partnership - rather than Company or Trust - legal framework.

See

http://lebleu.org/blog/2008/11/20/chris-cook-on-asset-based-finance...

This is the actual presentation I gave in Dublin which has additional explanation ....

http://www.feasta-multimedia.org/2008/Chris_Cook.mov

Whereas this presentation

http://www.slideshare.net/ChrisJCook/financing-energybeyond-peak-cr...

covered unitisation of energy.

In my view unitised energy is capable of becoming a global currency, replacing the dollar, while national currencies will be based on unitised land rental values.

The outcome will be a networked P2P "Clearing Union" similar to that proposed by Keynes at Bretton Woods, but created bottom up, not top down, and with no intermediary institutions.

-

-

Thank you Chris!

I love that you took the time to mingle with amateur "money designers"

We have good ideas when it comes to adding "meaning" to each transaction to direct money flows to be in sync with people's conscious values.

However, we (or speaking for myself) lack the deep perspective you have on existing alternative systems like Ripple (with whom I just had a brief exchange, and they did mention your work as a reference)

So I'll be looking at it and thinking about it.

Thanks again.

Marc

-

-

At this point, after the brainstorming about various 'thought models' and potentially related contexts, including the communication and collaboration contexts, I'm personally interested in feedback specific to the P2P currency model v0.5, as summarized under Objectives and detailed under the other sections in the previous post.

Money is obviously not a new invention, so I'm sure people have experimented with different definitions of it over the ages, so I'm also interested in finding out about any connections between aspects of the proposed currency model and other models from history or from the present.

-

-

Changes over v0.5 are limited to the Objectives section (#2) and the text within the accompanying Affinity Matrix image.

This version still lacks a comprehensive narrative/story under Context

Draft of P2P Currency Proposal: v0.6

Premise

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Context

The “P2P Social Currency” as it’s defined here is an ambitious idea, or “thought model,” for what we may end up with in 20 years from now, not a plan for today. Its goal is to stimulate and challenge people to think different.

Having said that, the concept of multidimensional currency, as described here, can be used with today’s money to move us closer towards a conscious economy.

This is only a draft and a fuller article is on the way.

Objectives

At the core of this proposal are these critical objectives:

1. Enable a lending model that rewards the lender without punishing the borrower by rewarding lending with seller credit points that give the lender higher rating among sellers (of goods and services.)

2. Encourage P2P energy production and energy abundance by tying centralized money creation to P2P energy production, such that those who produce energy locally (from natural, abundant sources like solar and wind) get the then-equivalent in P2P currency (or Peer Dollars) from the P2P Central Bank (or Peer Bank, the distributed utility company) while those who consume energy get to benefit from low-priced, abundant energy.

3. Provide a multi-dimensional value system for the purchase of goods or services instead of the 1-dimensional value system we have today, which is the numerical cost of goods and services. So that consumers become not just price conscious but more conscious about the other values, e.g. seller’s support for environment, seller’s use of organic ingredients, seller’s credit points (or generosity in lending), etc.

Original Idea

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of a daily/weekly/monthly amount of my own money that I let my kids use (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, e.g. buying $1,000 for $1,110, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated on how much you’ve lent others and how much time you give people to pay you back before you report their defaulting, i.e. the grace period, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

Follow-up and Clarification

I should add a clarification here that the conditions/rules imposed on the exchange of this new money (as defined in this post) do not last beyond the singular transaction. In other words, if I restrict my money to spend itself on organic food only, the grocery store that sells me the organic food will no longer have those rules imposed on the money I paid to them. They can enforce their on rules on it, whatever they may be, and then use it to buy stuff with, and so on…

As to the 1-dimensional value system that is imposed by the current definition of money, i.e. the numerical (or “price”) value, I think it is only a matter of time before this value system goes from being 1-dimensional to N-dimensional. The reason the value system that is imposed by the current definition of money is limited to just the numerical dimension, i.e. price, is because it is assumed that people do their own research/homework when trading with others and make their decision to trade based on that. What I’m suggesting is for the new money to have more than just a numerical value for a value system, i.e. other values that are programmed/re-programmed into it by every user of that money, thereby allowing the automation and streamlining of trading decisions.

The key argument here, besides the point about the need to abandon “interest,” is that the value system that is ‘explicit’ in the definition of money is 1-dimensional, i.e. the “price,” or numerical value, and there is no excuse for having this 1-dimensional value system when we have computers, the Internet and the ability to implement an _explicitly_ multi-dimensional value system as the basis for a new, social, P2P currency.

Another clarification is that if someone who has borrowed money does not pay back the money they get good will points taken out, much like the current credit rating system with the important exception that they can regain good will points (i.e. gain in their credit rating) by lending money to others rather than borrowing more money and paying interest on it.

The Origin of the Idea for Tying P2P Currency to P2P Energy

A very interesting idea suggested by Michel Bauwens of P2P Foundation is to derive the numerical value for this new money from the energy each person is able to produce (see: P2P energy.)

More on the Connection between P2P Currency and P2P Energy

There is a movement towards a Smart [Electric Distribution] Grid that allows individuals to produce electricity to power their homes and then send the extra capacity to the grid for others to use, and get paid for the energy they send into the grid.

The idea for Peer Energy Production will take some time to mature but there are already localized implementation of Smart Grid that allow businesses to play the role of a small electric utility.

So taking the Smart Grid further, we say that since solar energy is abundant then why not use this abundant resource that anyone can produce to be the basis for the new money. Meaning: if I can produce 100MegaWatts and push that into a ‘Peer Grid’ then the ‘Peer Bank’, which can print virtual Peer Dollars, would pay me 100 Peer Dollars or whatever amount, based on how much each Watt of energy goes for, which gets cheaper and cheaper the more energy is pushed into Peer Grid.

So the reason for tying money creation to energy creation is to encourage the generation of energy by people/businesses such that we end up with an abundance of energy as people exchange their excess locally generated energy for Peer Dollars, which, in the envisioned P2P Economy, they can use to buy anything with or lend to others.

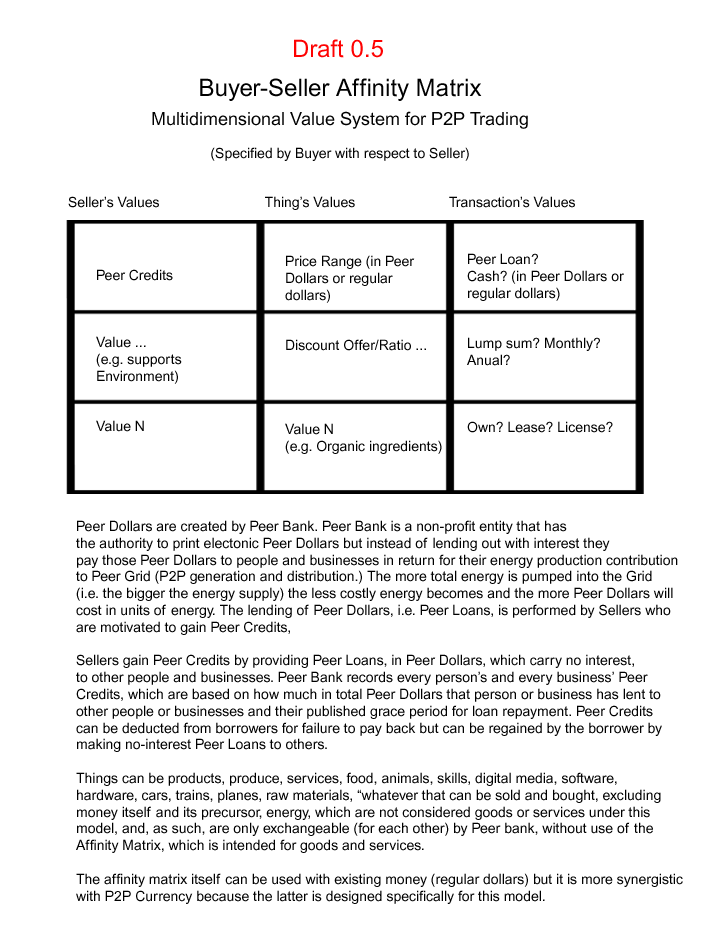

Peer Loans

Why do we need to lend? Because we need money to flow in the system, like blood flowing in our veins. No blood/money flowing means death of the system. Lending is needed beyond the exchange of goods/services for money. That’s because in order to create or buy goods/services people need money and lending allows people to have more money than they can have from their labor. In other words, the increased flow of money through lending is important to the healthy functioning and growth of the system. The problem with “interest” being the incentive for lending today is that it’s used to derive more money for the lender, which has nothing wrong with it, at the expense of the borrower, which is wrong.

That is to say that “interest” rewards lenders and punishes borrowers. What we need is a replacement of interest as an incentive for lending. Something that would reward lender with punishing the borrower.

If someone lends money and instead of getting more money back they get good will points (Peer Credits) then more people will buy from that lender (the one with most Peer Credits), so the lender makes more money by selling *more* products and services, not by simply sitting back and collecting from borrowers.

Applicable Today

All concepts here can be implemented today using today’s money. There is no need to wait for P2P Energy/Peer Dollars. The only benefit (big benefit) of Peer Dollars is that they encourage P2P energy production. The model itself as described here is beneficial with or without P2P Energy/Peer Dollars, and can be applied today.

See: Buyer-Seller Affinity Matrix: Multidimensional Value System for P2P...

Feedback

I’m interested in feedback specific to the P2P currency model v0.5, as summarized under Objectives and detailed under the other sections in the previous post.

Money is obviously not a new invention, so I’m sure people have experimented with different definitions of it over the ages, so I’m also interested in finding out about any connections between aspects of the proposed currency model and other models from history or from the present.

{kind=link}

© 2024 Created by Josef Davies-Coates.

Powered by

![]()