The Foundation for Peer to Peer Alternatives

P2P Social Currency (Money 2.0)

Hi there,

I would like to present the ideas in this article below for discussion with folks on this forum.

The article itself is something I put together over night but I have been sitting with the ideas for a couple years now.

I could be a lot more elaborate in my presentation of these ideas, but I thought I'd run it by other curiously minded folks, to have some critical feedback points, prior to putting significant energy into it...

With that said, please enjoy and comment as appropriate.

Original URL: http://evolvingtrends.wordpress.com/2008/10/21/p2p-social-currency-...

P2P Social Currency (Money 2.0)

October 21, 2008 at 7:18 pm

Premise:

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Dialog:

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of money that I give to my kids (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

In my opinion, the concept of “credit” and “credit rating” is good but the concept of interest is not. What I mean is that people and businesses should have a credit rating but it should be tied to something other than their ability to pay interest on money borrowed.

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated by how much you’ve lent others and how much time you’ve given people to pay you back, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

I would like to present the ideas in this article below for discussion with folks on this forum.

The article itself is something I put together over night but I have been sitting with the ideas for a couple years now.

I could be a lot more elaborate in my presentation of these ideas, but I thought I'd run it by other curiously minded folks, to have some critical feedback points, prior to putting significant energy into it...

With that said, please enjoy and comment as appropriate.

Original URL: http://evolvingtrends.wordpress.com/2008/10/21/p2p-social-currency-...

P2P Social Currency (Money 2.0)

October 21, 2008 at 7:18 pm

Premise:

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Dialog:

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of money that I give to my kids (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

In my opinion, the concept of “credit” and “credit rating” is good but the concept of interest is not. What I mean is that people and businesses should have a credit rating but it should be tied to something other than their ability to pay interest on money borrowed.

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated by how much you’ve lent others and how much time you’ve given people to pay you back, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

Views: 2105

Replies to This Discussion

-

Permalink Reply by Sepp Hasslberger on

-

"Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?"

Yes, and it ideally should be an online virtual world (or online community?) that is based on peer-to-peer, open source software (discussed here), rather than one of the commercial online communities available today. To be sure, such a virtual world does not exist yet, but the linked article shows that some people are thinking how to bring it about.

One point that will be difficult, I think, is the link to p2p energy production. At least initially, the community will not be compact enough to enable direct exchange of the energy, so the peer bank will have to be virtual as well, to start out with, and somehow people's production (and pushing into the grid) of energy will have to be documented for the peer bank to be able to start issuing the currency. A difficulty, but not impossible to overcome.

-

Permalink Reply by Evolving Trends on

-

I agree with all your assessments.

I'm personally interested simulation/virtualization of the model as opposed to deferring certain objectives until they become practical/feasible, but I would definitely support social trading software that implements this in parts/stages.

Simulation allows us to experiment :) and see..

-

-

draft v0.07

Changes:

- Added a note on the need for hourly cap on energy production per producer (see last paragraph of section on Energy and Currency)

- Added a note on the need for anti-aggregation provision to disallow emergent master-slave behavior where one person or entity end up running a colony of P2P energy producing peers.

Notes:

This version still lacks a comprehensive narrative/story under Context.

Next version will include segments of discussions on Demurrage and the asymmetric nature of the Affinity Matrix.

Draft of P2P Currency Proposal: v0.07

Premise

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Context

The “P2P Social Currency” as it’s defined here is an ambitious idea, or “thought model,” for what we may end up with in 20 years from now, not a plan for today. Its goal is to stimulate and challenge people to think different.

Having said that, the concept of multidimensional currency, as described here, can be used with today’s money to move us closer towards a conscious economy.

This is only a draft and a fuller article is on the way.

Objectives

At the core of this proposal are these critical objectives:

1. Enable a lending model that rewards the lender without punishing the borrower by rewarding lending with seller credit points that give the lender higher rating among sellers (of goods and services.)

2. Encourage P2P energy production and energy abundance by tying centralized money creation to P2P energy production, such that those who produce energy locally (from natural, abundant sources like solar and wind) get the then-equivalent in P2P currency (or Peer Dollars) from the P2P Central Bank (or Peer Bank, the distributed utility company) while those who consume energy get to benefit from low-priced, abundant energy.

3. Provide a multi-dimensional value system for the purchase of goods or services instead of the 1-dimensional value system we have today, which is the numerical cost of goods and services. So that consumers become not just price conscious but more conscious about the other values, e.g. seller’s support for environment, seller’s use of organic ingredients, seller’s credit points (or generosity in lending), etc.

Original Idea

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of a daily/weekly/monthly amount of my own money that I let my kids use (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, e.g. buying $1,000 for $1,110, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated on how much you’ve lent others and how much time you give people to pay you back before you report their defaulting, i.e. the grace period, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

Follow-up and Clarification

I should add a clarification here that the conditions/rules imposed on the exchange of this new money (as defined in this post) do not last beyond the singular transaction. In other words, if I restrict my money to spend itself on organic food only, the grocery store that sells me the organic food will no longer have those rules imposed on the money I paid to them. They can enforce their on rules on it, whatever they may be, and then use it to buy stuff with, and so on…

As to the 1-dimensional value system that is imposed by the current definition of money, i.e. the numerical (or “price”) value, I think it is only a matter of time before this value system goes from being 1-dimensional to N-dimensional. The reason the value system that is imposed by the current definition of money is limited to just the numerical dimension, i.e. price, is because it is assumed that people do their own research/homework when trading with others and make their decision to trade based on that. What I’m suggesting is for the new money to have more than just a numerical value for a value system, i.e. other values that are programmed/re-programmed into it by every user of that money, thereby allowing the automation and streamlining of trading decisions.

The key argument here, besides the point about the need to abandon “interest,” is that the value system that is ‘explicit’ in the definition of money is 1-dimensional, i.e. the “price,” or numerical value, and there is no excuse for having this 1-dimensional value system when we have computers, the Internet and the ability to implement an _explicitly_ multi-dimensional value system as the basis for a new, social, P2P currency.

Another clarification is that if someone who has borrowed money does not pay back the money they get good will points taken out, much like the current credit rating system with the important exception that they can regain good will points (i.e. gain in their credit rating) by lending money to others rather than borrowing more money and paying interest on it.

The Origin of the Idea for Tying P2P Currency to P2P Energy

A very interesting idea suggested by Michel Bauwens of P2P Foundation is to derive the numerical value for this new money from the energy each person is able to produce (see: P2P energy.)

More on the Connection between P2P Currency and P2P Energy

There is a movement towards a Smart [Electric Distribution] Grid that allows individuals to produce electricity to power their homes and then send the extra capacity to the grid for others to use, and get paid for the energy they send into the grid.

The idea for Peer Energy Production will take some time to mature but there are already localized implementation of Smart Grid that allow businesses to play the role of a small electric utility.

So taking the Smart Grid further, we say that since solar energy is abundant then why not use this abundant resource that anyone can produce to be the basis for the new money. Meaning: if I can produce 100MegaWatts and push that into a ‘Peer Grid’ then the ‘Peer Bank’, which can print virtual Peer Dollars, would pay me 100 Peer Dollars or whatever amount, based on how much each Watt of energy goes for, which gets cheaper and cheaper the more energy is pushed into Peer Grid.

So the reason for tying money creation to energy creation is to encourage the generation of energy by people/businesses such that we end up with an abundance of energy as people exchange their excess locally generated energy for Peer Dollars, which, in the envisioned P2P Economy, they can use to buy anything with or lend to others.

There may need to be a cap put in place on how much energy a given party can produce so as not to allow one party or few parties to pump so much energy into Peer Grid as to bring energy price down for all other producers. Maybe a maximum on the amount of energy you can pump into the grid per hour has to be calculated based on demand, to stabilize the price of energy, and the currency which is based on it.

There probably also needs to be an anti-aggregation provision (in the model) to disallow emergent master-slave behavior where one person or entity end up running a colony of P2P energy producing peers.

Peer Loans

Why do we need to lend? Because we need money to flow in the system, like blood flowing in our veins. No blood/money flowing means death of the system. Lending is needed beyond the exchange of goods/services for money. That’s because in order to create or buy goods/services people need money and lending allows people to have more money than they can have from their labor. In other words, the increased flow of money through lending is important to the healthy functioning and growth of the system. The problem with “interest” being the incentive for lending today is that it’s used to derive more money for the lender, which has nothing wrong with it, at the expense of the borrower, which is wrong.

That is to say that “interest” rewards lenders and punishes borrowers. What we need is a replacement of interest as an incentive for lending. Something that would reward lender with punishing the borrower.

If someone lends money and instead of getting more money back they get good will points (Peer Credits) then more people will buy from that lender (the one with most Peer Credits), so the lender makes more money by selling *more* products and services, not by simply sitting back and collecting from borrowers.

Applicable Today

All concepts here can be implemented today using today’s money. There is no need to wait for P2P Energy/Peer Dollars. The only benefit (big benefit) of Peer Dollars is that they encourage P2P energy production. The model itself as described here is beneficial with or without P2P Energy/Peer Dollars, and can be applied today.

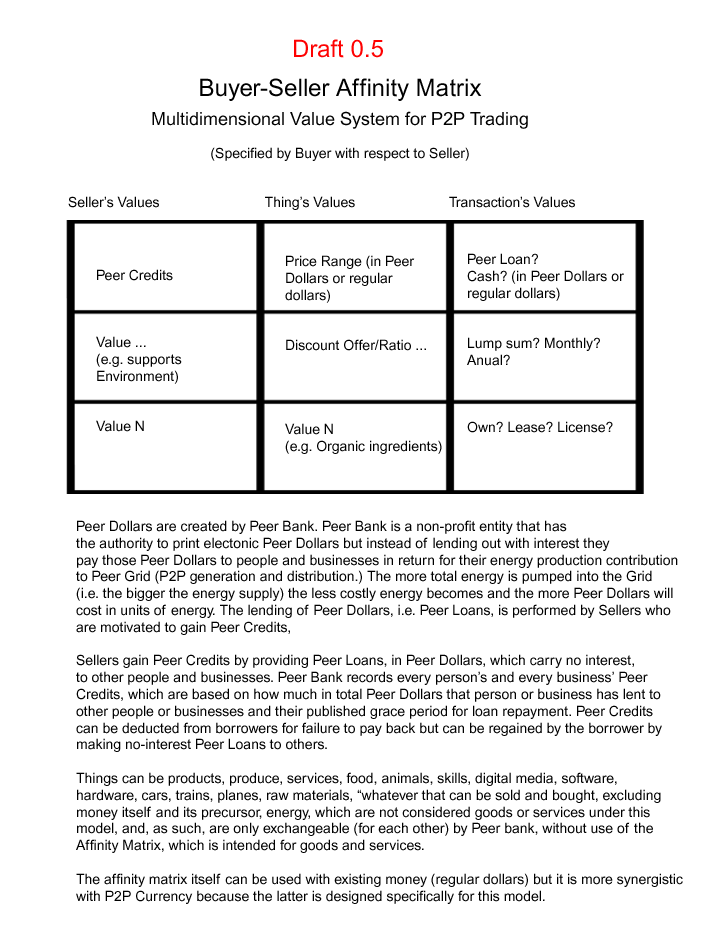

See: Buyer-Seller Affinity Matrix: Multidimensional Value System for P2P...

Feedback

I’m interested in feedback specific to the P2P currency model v0.5, as summarized under Objectives and detailed under the other sections in the previous post.

Money is obviously not a new invention, so I’m sure people have experimented with different definitions of it over the ages, so I’m also interested in finding out about any connections between aspects of the proposed currency model and other models from history or from the present.

{kind=link}

-

-

"So the reason for tying money creation to energy creation is to encourage the generation of energy by people/businesses such that we end up with an abundance of energy as people exchange their excess locally generated energy for Peer Dollars..."

"There may need to be a cap put in place on how much energy a given party can produce so as not to allow one party or few parties to pump so much energy into Peer Grid as to bring energy price down for all other producers."

These two statements seem to be contradictory.

The object of a tie between money and energy is to promote the abundant availability of energy produced in a distributed way. Abundant energy tends to be cheap.

But there is a self-regulating mechanism at work here. Energy production implies investment to build and maintain physical equipment. As energy gets cheaper, the investment costs tend to exceed profit to be made and thus tend to limit production. So there is a negative feedback loop that would tend towards a stable equilibrium condition and make an artificial cap superfluous.

Also, in my opinion, the more arbitrary rules you need in a money system to enforce certain behavior, the more possible breakdown points you have. People will figure out ways to get around the rules and you end up with an unstable system in the long run. I would definitely be very reluctant to introduce purely arbitrary rules such as a numeric cap on energy production.

-

-

I had thought about the negative feedback loop as you stated it prior to thinking about the cap idea and the reason for the cap idea was that it is possible for someone to continue investing in energy infrastructure to starve out the new entrants. Mean behavior, greed, and bad behavior in general is possible and you cannot guarantee that men turn into wise angels because the system is designed to allow them to do that. It's true that most will, but some won't.

Another thing is that the statements on abundance and caps are not contradictory, abundance does not come from 1 person providing all the energy, which is an extreme situation that can happen. Bill Gates or whomever rich nation can decide to invest heavily (beyond the point of positive return) into energy infrastructure, driving energy price to near zero and thus starving new entrants and creating single source dependence.

That's why dynamic regulation of energy price and peer caps (per hour) are necessary.

:)

Let me know where I'm wrong...

As to the fact that too many arbitrary rules create too many break points, I could not agree more before the current financial crisis. The thought was "deregulate." People want to demonize Republicans in US for pushing for deregulation and now European Union and US are tangled in debate over how much regulation (read: arbitrary rules)

Some are needed. I had the opposite opinion, i.e. that none are needed and the market should self regulate. But not after the mess we got into. Greespan (to some the devil) said that he had a flow in his thinking about how the world works, and this flaw is that he assumed people will do good for themselves and others, and not act exceedingly selfish. He was wrong of course, as bankers wanted to be paid commissions to buy new mansions and Ferraris at the expense of destabilizing their own banks.

Greenspan was a champion of deregulations, a purist.

There is no way that your good ideals for the world are to be compared to Greenspan's ideals for a completely different kind of world, but my ideals before the current meltdown was to have freedom, no regulation and unfortunately that led to anarchic behavior and exceedingly selfish behavior.

So arbitrary rules (regulations) are being introduced across the board now, up and down the stack, like never before :)

It's crazy.

You'd want as few arbitrary rules as possible. But you don't want none.

It's like the little amount of salt in food that keeps the food from going bad

-

-

On the asymmetric nature of the buyer-seller affinity matrix:

This is probably the most interesting point in the debate ....

Given that everyone in a p2p economy is by definition both a seller and a buyer or even a "Prosumer" (i.e. Producer + Consumer) which is a step beyond "seller" (as seller can be just a reseller of what others produce)

If goods/services were universally guaranteed to be exchangeable for money then sellers should be able to decide whose buyer's money to take., as they will have that choice/power.

But goods/services may be bad/defective and their value is subjective not objective and as such they cannot be guaranteed to be exchangeable for money. In other words, a seller does not have as much power as a buyer... but a seller is also a buyer. The difference in power is with respect to the role not with respect to the person/entity/peer.

Money is guaranteed to be exchangeable for goods/services. So the disposer of the money (the buyer) has the power to decide which goods/services to spend their money on.

As for lenders the only thing they should look at (from the affinity matrix) is the credit points of the borrower.

Fuller discussion possible ...

-

-

Draft of P2P Currency Proposal: v0.08

Changes:

- Added section: Credit Points For Lenders

- Added section: Credit Points For Borrowers

- Added section: Affinity Matrix for P2P Trading

- Added exception for trading energy (and updated corresponding text in Affinity Matrix image)

Notes:

This version still lacks a comprehensive narrative/story under Context.

Premise

One of the foundational elements of society is the definition of money.

Changing how money is defined will change society.

Context

The “P2P Social Currency” as it’s defined here is an ambitious idea, or “thought model,” for what we may end up with in 20 years from now, not a plan for today. Its goal is to stimulate and challenge people to think different.

Having said that, the concept of multidimensional currency, as described here, can be used with today’s money to move us closer towards a conscious economy.

This is only a draft and a fuller article is on the way.

Objectives

At the core of this proposal are these critical objectives:

1. Enable a lending model that rewards the lender without punishing the borrower by rewarding lending with seller credit points that give the lender higher rating among sellers (of goods and services.)

2. Encourage P2P energy production and energy abundance by tying centralized money creation to P2P energy production, such that those who produce energy locally (from natural, abundant sources like solar and wind) get the then-equivalent in P2P currency (or Peer Dollars) from the P2P Central Bank (or Peer Bank, the distributed utility company) while those who consume energy get to benefit from low-priced, abundant energy.

3. Provide a multi-dimensional value system for the purchase of goods or services instead of the 1-dimensional value system we have today, which is the numerical cost of goods and services. So that consumers become not just price conscious but more conscious about the other values, e.g. seller’s support for environment, seller’s use of organic ingredients, seller’s credit points (or generosity in lending), etc.

Original Idea

If we had a networked, programmable currency then I could tell my money to exchange itself only for goods/services that are made by vendors who care about the planet AND who have donated to my chosen candidate for President.

I can be as particular as I want and my money should do the figuring out of whom to pay itself to, based on rules I supply, and based on information it can access about the parties I’m trading with.

Another example for networked, programmable currency is to enforce rules on the spending of a daily/weekly/monthly amount of my own money that I let my kids use (luckily no kids yet) so they don’t buy food that contains unhealthy ingredients.

The new networked, programmable money should abandon the idea of paying interest on borrowed money. There is so much debt in the system that it would take decades to get rid of it and return the economy to normal functioning. The interest on debt is like bad cholesterol. While it fattens the economy, it ultimately clogs the global economic arteries and can lead to economic failure, as it has done (see: global economic meltdown 2008.)

If you lend money to someone, where that someone is chosen per the particular criteria you’ve programmed into your money, you should be able to get your money back and get “good will” points that would replace today’s “hamster wheel” concept of credit rating, which was designed to encourage people to buy money with money, e.g. buying $1,000 for $1,110, which is not only retarded but gives value to money from nowhere. Instead of being rated on your timeliness in paying back money borrowed + interest, you should be rated on how much you’ve lent others and how much time you give people to pay you back before you report their defaulting, i.e. the grace period, and this rating, e.g. your “good will” points, becomes your credit rating. This way people can dictate that their money is to be exchanged for goods/services only from providers with N “good will” points or more.

Maybe a good place to try this P2P Social Currency (or “Money 2.0″) would be in an online virtual world?

Follow-up and Clarification

I should add a clarification here that the conditions/rules imposed on the exchange of this new money (as defined in this post) do not last beyond the singular transaction. In other words, if I restrict my money to spend itself on organic food only, the grocery store that sells me the organic food will no longer have those rules imposed on the money I paid to them. They can enforce their on rules on it, whatever they may be, and then use it to buy stuff with, and so on…

As to the 1-dimensional value system that is imposed by the current definition of money, i.e. the numerical (or “price”) value, I think it is only a matter of time before this value system goes from being 1-dimensional to N-dimensional. The reason the value system that is imposed by the current definition of money is limited to just the numerical dimension, i.e. price, is because it is assumed that people do their own research/homework when trading with others and make their decision to trade based on that. What I’m suggesting is for the new money to have more than just a numerical value for a value system, i.e. other values that are programmed/re-programmed into it by every user of that money, thereby allowing the automation and streamlining of trading decisions.

The key argument here, besides the point about the need to abandon “interest,” is that the value system that is ‘explicit’ in the definition of money is 1-dimensional, i.e. the “price,” or numerical value, and there is no excuse for having this 1-dimensional value system when we have computers, the Internet and the ability to implement an _explicitly_ multi-dimensional value system as the basis for a new, social, P2P currency.

The Origin of the Idea for Tying P2P Currency to P2P Energy

A very interesting idea suggested by Michel Bauwens of P2P Foundation is to derive the numerical value for this new money from the energy each person is able to produce (see: P2P energy.)

More on the Connection between P2P Currency and P2P Energy

There is a movement towards a Smart [Electric Distribution] Grid that allows individuals to produce electricity to power their homes and then send the extra capacity to the grid for others to use, and get paid for the energy they send into the grid.

The idea for Peer Energy Production will take some time to mature but there are already localized implementation of Smart Grid that allow businesses to play the role of a small electric utility.

So taking the Smart Grid further, we say that since solar energy is abundant then why not use this abundant resource that anyone can produce to be the basis for the new money. Meaning: if I can produce 100MegaWatts and push that into a ‘Peer Grid’ then the ‘Peer Bank’, which can print virtual Peer Dollars, would pay me 100 Peer Dollars or whatever amount, based on how much each Watt of energy goes for, which gets cheaper and cheaper the more energy is pushed into Peer Grid.

So the reason for tying money creation to energy creation is to encourage the generation of energy by people/businesses such that we end up with an abundance of energy as people exchange their excess locally generated energy for Peer Dollars, which, in the envisioned P2P Economy, they can use to buy anything with or lend to others.

There may need to be a cap put in place on how much energy a given party can produce so as not to allow one party or few parties to pump so much energy into Peer Grid as to bring energy price down for all other producers. Maybe a maximum on the amount of energy you can pump into the grid per hour has to be calculated based on demand, to stabilize the price of energy, and the currency which is based on it.

There probably also needs to be an anti-aggregation provision (in the model) to disallow emergent master-slave behavior where one person or entity end up running a colony of P2P energy producing peers.

Peer Loans

Why do we need to lend? Because we need money to flow in the system, like blood flowing in our veins. No blood/money flowing means death of the system. Lending is needed beyond the exchange of goods/services for money. That’s because in order to create or buy goods/services people need money and lending allows people to have more money than they can have from their labor. In other words, the increased flow of money through lending is important to the healthy functioning and growth of the system. The problem with “interest” being the incentive for lending today is that it’s used to derive more money for the lender, which has nothing wrong with it, at the expense of the borrower, which is wrong.

That is to say that “interest” rewards lenders and punishes borrowers. What we need is a replacement of interest as an incentive for lending. Something that would reward lender with punishing the borrower.

If someone lends money and instead of getting more money back they get good will points (Peer Credits) then more people will buy from that lender (the one with most Peer Credits), so the lender makes more money by selling *more* products and services, not by simply sitting back and collecting from borrowers.

Credit Points For Lenders

To encourage the flow of capital in the P2P economy, lenders need to have an incentive.

The incentive in this model is based on the assumption that in the P2P economy everyone is a buyer and a seller (of goods and/or services.)

The idea is to give lenders credit points (Peer Credits) that rank them higher as sellers when buyers search for goods or services that they happen to offer. The number of Peer Credits a lenders gets is based on how much they’ve loaned to others and their standard grace period (for loan repayment.)

Credit Points for Borrowers

When borrowers borrow money (Peer Dollars) under this model and repay it on time they do not gain credit points. The borrower’s benefit comes from having to pay no interest on money borrowed. If the borrower does not pay the borrowed amount after the grace period they get negative Peer Credits. However, the borrower can come out of a negative Peer Credit rating simply by lending lending money to someone else, after paying back the money they owe. While this may sound pessimistic for such borrowers, the ease with which people can accumulate money through the local production of energy (by pumping excess locally generated energy into Peer Grid and receiving the then-equivalent in Peer Dollars) should make it viable for borrowers to recover from negative Peer Credit rating.

The amount a borrower can borrow is directly tied to the number of Peer Credits they have, and since Peer Credits can only be obtained via the act of lending, this encourages people to keep lending and at the same time forgives people who fail to pay back borrowed money by giving them a chance to make money (by pumping excess locally produced energy back to Peer Grid) and then lend some of that money to someone else and keep doing that until they’ve established good Peer Credit rating.

The way the current system works is by penalizing borrowers who default without giving them an easy enough way to recover from their defaulting position. Furthermore, paying back the lender, after defaulting never helps the credit score, and borrowers are forced to borrow more rather than lend more because it’s assumed that money is scarce and cannot be peer produced, which is not the case in this proposed model) and borrowing more has the effect of concentrating money and power in the hands of the biggest lenders, instead of encouraging every borrower to become a lender, too, which is what this model aspires to do and which creates money for all puts power with the whole.

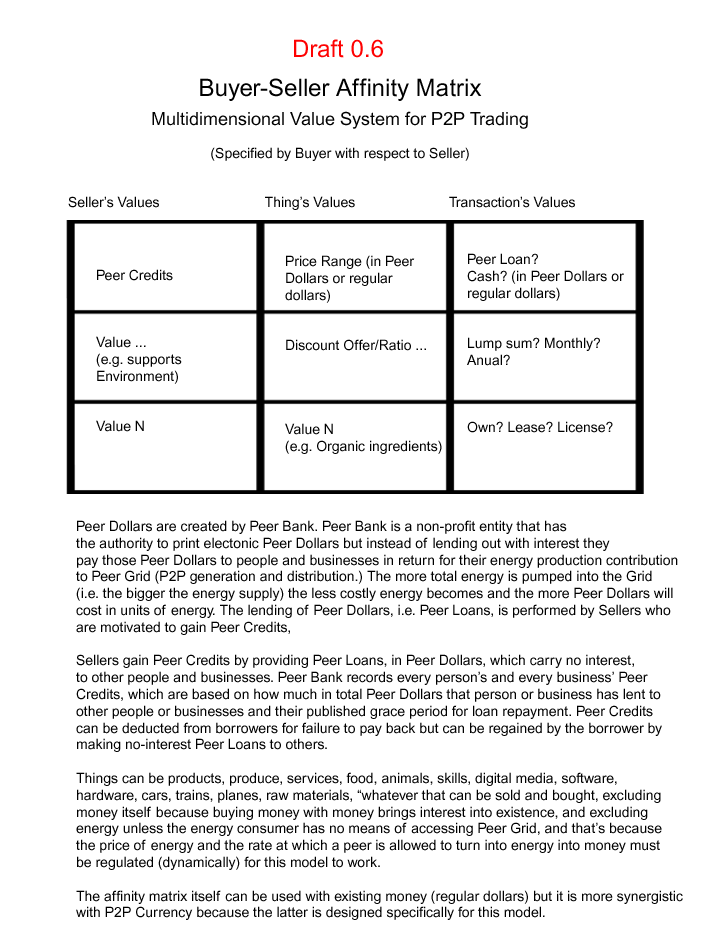

Affinity Matrix for P2P Trading

The Affinity Matrix allows the explicit definition of a multidimensional value system per each transaction involving Peer Dollars, but it should also be usable with conventional currency.

The affinity is asymmetric in nature, i.e. specified by buyer with respect to seller, and it applies only to goods and services, which do not include money because you shouldn’t be able to buy money with money as money as that would be equal to ‘interest,’ and which do not include or energy, except where the energy consumer cannot tap into Peer Grid, and that’s because the price of energy and the rate at which a peer is allowed to turn into energy into money must be regulated (dynamically) for this model to work.

The reason the affinity is unidirectional from buyer to seller is because the buyer holds money and the seller holds goods and/or services. The money has an objective value, i.e. the price, ($5 is $5 is $5) and the goods/service has a subjective value. The value of something, other than money, is ultimately subjective. In fact, that is why the Affinity Matrix is needed, i.e.: to add explicit subjective values to goods and services.

So given that goods and services have a subjective value (or values) and money has an objective value (price) the seller (or holder of goods and services) is not in position to dictate which buyer’s money they like to take. The reason being that you can’t have power in deciding a trade without having objective value in what you’re offering to trade. Your goods and services can have an extremely high subjective value but you can’t go to the bank and exchange them for money. If no one wants to buy your goods and services, no matter how good they are, you can’t make any money on them. Furthermore, if buyers decide to sit out the shopping season you can’t turn your goods and services into money. The buyer, on the other hand, is the holder of the money and given money has an objective value, which means that there is always someone willing to take it in return for goods or services. Therefore, the buyer has the power to dictate which seller’s goods and services they want to exchange their money for. The seller doesn’t except in cases where they have a monopoly on goods or services and those goods and services happen to be in demand. The seller is otherwise just happy to find a buyer to make a living off their trade. But if your goods and services are in high demand then you can decide which buyer’s money to take and the way to do that in a fair way is to offer it to the highest bidder. Otherwise, you risk starting a fight amongst the buyers and between buyers and yourself. Under the proposed model, sellers can price their items as high as they want and if that item is scarce or in very high demand then buyers will likely pay the price, assuming the seller and their goods and services have a high enough degree of affinity with the buyers’ values or the buyers, under conditions of scarcity, just don’t care about enforcing their values.

See: Buyer-Seller Affinity Matrix: Multidimensional Value System for P2P...

Open Feedback Request

Money is obviously not a new invention, so I’m sure people have experimented with different definitions of it over the ages, so I'm interested in finding out about any connections between aspects of this proposed P2P currency model and other models from history or from the present.

All feedback, request for clarification or comment, good or bad, is very welcome.

{kind=link}

-

-

I may go ahead and develop this version 0.08 as a simulation but that would amount to a major effort. The good news is that the simulation can be turned into a game where the objective is to accumulate the most Peer Credits or something like that.

The model by now has some good ideas and it's well explained for the most part, and can be explained better as I get more counter arguments and comments, but I feel a great need to be challenged in my arguments, and proven wrong where possible, before I'd invest any more work into it.

The game sounds pretty good to me, but even then I'd still need to see all the arguments I've made so far be scrutinized with no mercy... hopefully by someone with vested interest in the current system or by someone with vested interest in a far more radical/revolutionary model

Not to say that a third grader won't be able to unravel it with some good luck :)

Anyway, it still needs to be debated inside/out

-

Permalink Reply by Dante-Gabryell Monson on

-

Hi Marc - it might eventually be interesting to add

the Draft of P2P Currency Proposal

to

http://openmoney.ning.com/

-

-

Yes, once it received enough vetting/debate over here

But I'm inclined to also keep it HERE because at it's core is the idea of P2P economics

The biggest philosophical issues I've ran into here and on email chat with Sepp and other fellow members here, is the following:

1. If we establish heaven, everybody will behave nicely and balance their interest with that of the whole. Another similar way of stating this: if we develop a well-designed system that allows everyone to do well and by consequence enable the whole system to do well then we won't have exceedingly selfish behavior or anarchic behavior that can bring such "pure thought", idealistic system crashing down.

2. Greed and bad behavior can be eliminated by designing an idealistic, open, or totally free (regulation free) environment.

"salt" in your food is bad for you but salt in the right amount is good for you and good for your food. The food being the system here. Without salt it will go bad. You can put any one of 100 other preserving components but at the end of the day it is something you add to your food to keep it from getting bad, it is not food in itself.

Same thing with regulations. They are not food (they are not part of the system that we call "economy") they are needed in small amount to keep the system from collapsing and the reason is that you cannot eliminate bad behavior. You can only be resilient to it.

So this opens up a pandora's box of arguments but it's the most important part of the debate.

Even though Greenspan maybe the devil to some, his admission that free markets need regulation is outstanding. As P2P advocates we tend to advocate total freedom and ideal designs (pure thought) .. something like Plato imagined: mathematical truth. Unfortunately as Godel would later prove, there is no such thing. It is possible that you cannot attain axiomatic completeness or consistency. So there is uncertainty even in mathematics (even post Bernard Russel, with set theory and axiom of choice etc.) In other words, a logical flaw can creep up in the best designed models. Thus, logic itself is not infallible.

In other words, the reason to admit that things can go wrong in the best designed logical models is not just wise but it has been proven.

So if things CAN GO WRONG, shouldn't we have safeguards/regulations/arbitrary rules even for the most logically well designed model?

:) ?

-

-

Let me summarize the above in a better way:

I am arguing against the following two assumptions:

1) if we design a logically perfect, mathematically beautiful system then people will do what is logical rather than taking purposefully or unknowingly illogical actions

2) if people do what is logical then we can be sure that a logically perfect system will not have axiomatic incompleteness or inconsistency, i.e. that 'logic' itself is infallible.

#1, in a way, refers to nature vs nurture ... the problem is doing things logically has more to do with human capacity to compute logical outcomes than it does with nature or nurture.... some people, including myself, will often fail to compute logical outcomes or don't even care... be it for sake of disruption, risk taking or whatever 'thrill' or random cause, e.g. lack of sleep, stress, fear, anger, etc, which is why it's important to address our feelings about the problem before trying to solve it.

#2 has to do with the idea of mathematical truth, i.e. that logic is guaranteed to be infallible. Godel proved that and it persisted post Bernard Russel in the set theory.

So if we can't guarantee everything will work fine per whatever logic we have dictated into the model then shouldn't we have some safeguards? After all, even if everyone did what's logical (all the time or most of the time) our logic itself is never guaranteed to be infallible, i.e. there is a chance that we will have to continuously update our axiomatic system, so why not start with a set of ethically positive axioms and accept from the beginning that we need to include axioms that constrain people to do things logically and then keep adding to those axioms as necessary until we feel we've reached a safe enough model and can tolerate the remaining extremely small probabilities of things going wrong.

That's my thinking. Feel free to tear it apart.

This is definitely the most interesting point in the debate.

-

-

The conclusion I just underlined/bolded is the "design approach" for the model which should be highlighted in the proposal:

Given that people will not always behave logically and given that logic itself is not infallible, why not start with a set of ethically positive axioms and accept from the beginning that we need to include axioms that constrain people to do things logically and then keep adding to those axioms as necessary until we feel we've reached a safe enough model and can tolerate the remaining extremely small probabilities of things going wrong.

This is really the 'design approach' and its great that it came out during the discussion... I would have never thought about the meta-logical design approach or the design behind the design on my own, at least not so quickly... so Thank You!

That's really where I wanted to park this discussion and take a long walk to figure out what it is we're really arguing about here: freedom of choice? mathematical beauty/truth? fear vs. hope?

There are many ways to frame this.

:)

© 2024 Created by Josef Davies-Coates.

Powered by

![]()